Getting your first car insurance quote as a young driver can feel like a punch to the gut. £3,000 a year?

Seriously?

Don’t panic. You’re not doomed to pay through the nose forever.

I’ve seen young drivers slash their premiums by thousands using these proven strategies. Some work immediately. Others take a bit of patience.

Ready to fight back against those sky-high quotes?

Contents

Choose Your First Car Wisely

Your car choice makes or breaks your insurance costs. That souped-up Corsa might look amazing, but it’ll cost you significantly more.

Insurance companies group cars into categories 1-50, administered by Thatcham Research. The lower the number, the cheaper your insurance.

A Volkswagen Up! sits in group 1.

A BMW M3? Try group 50.

Young drivers should stick to groups 1-10. Think Ford Ka, Nissan Micra, or Vauxhall Corsa (the basic models, not the sporty ones).

Small engines matter too. A 1.0-litre engine will cost way less to insure than a 1.6-litre.

Insurance companies know bigger engines mean more temptation to drive fast.

Add an Experienced Named Driver

This one’s excellent for reducing costs.

Adding a parent or guardian as a named driver can cut your premium substantially, especially for drivers aged 17-25 when the risk differential is greatest.

But here’s the catch – they actually need to drive the car sometimes.

If they never touch the keys, that’s called “fronting” and it’s fraud.

Make sure the main driver (that’s you) is listed correctly. The person who drives the car most should be the main driver. No exceptions.

Your mum driving to the shops once a month? Perfect.

Never letting her near your car? That could cause problems with your insurer.

Consider Black Box Insurance

Black box insurance gets a bad reputation, but it can save young drivers serious money.

Research shows telematics policies provide 8-60% savings, with average annual savings of £150-£700.

The device monitors your driving – speed, braking, cornering, and when you drive. Drive well, pay less. It’s that simple.

Black box policies provided the most affordable quotes for 70% of drivers aged 17-20. Young drivers with these policies pay an average of £1,483 compared to £1,954 for standard policies.

Most insurers set a curfew (usually 11pm-6am). Stick to it.

Avoid harsh braking and acceleration. Take corners smoothly.

The monitoring feels strange at first, but you’ll quickly forget it’s there.

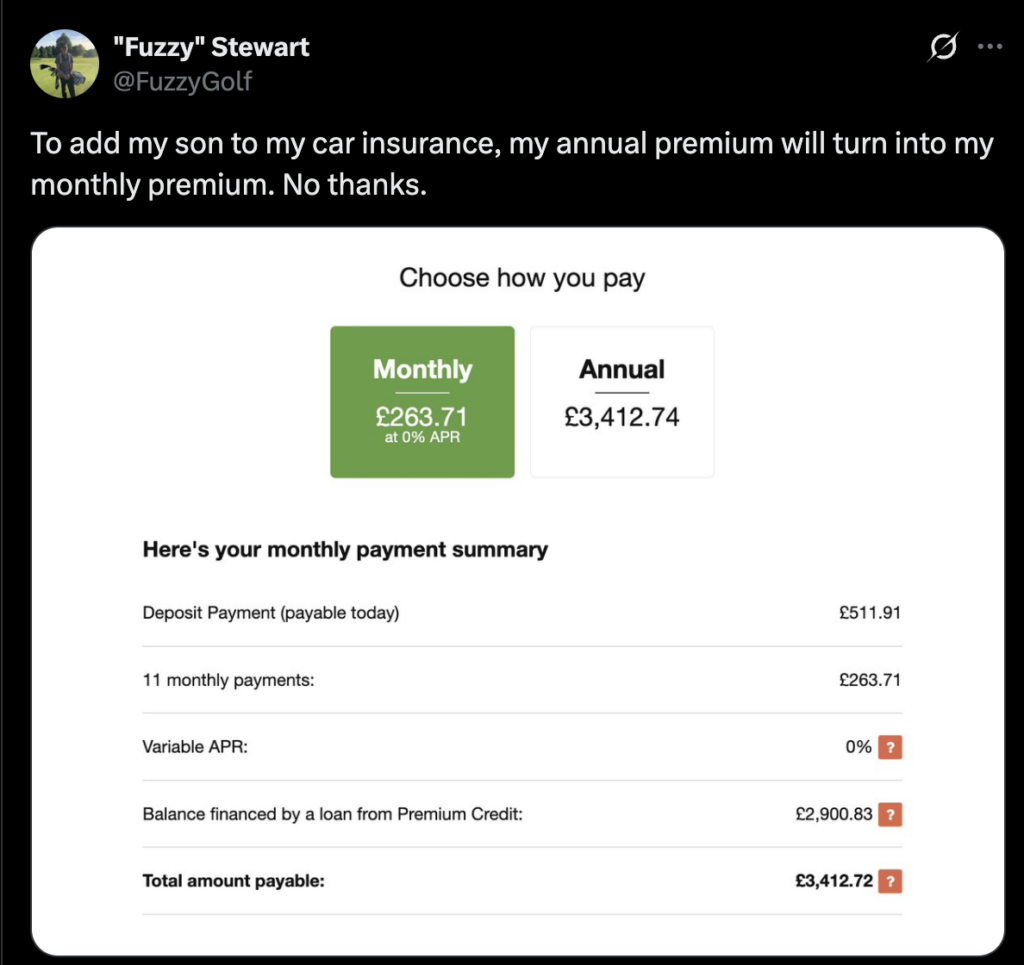

Pay Annually, Not Monthly

Monthly payments seem easier on your wallet, but they cost more overall. Insurance companies charge interest on monthly plans – typically 15.9% to 39.11% APR across UK insurers.

The average APR is 23.37% based on research across 27 providers.

A £1,200 annual policy might cost £1,320 when paid monthly. That’s £120 extra for the convenience.

The average annual savings from paying yearly is £249.

If you can’t afford the lump sum, ask family for a loan. Paying them back interest-free beats paying the insurance company’s markup.

Some insurers like NFU Mutual and Hiscox offer 0% interest monthly plans, but they’re rare.

Build Your No Claims Bonus

Your no claims bonus is extremely valuable. UK insurers offer consistent discount structures across the market:

- One year: 20-30% discount

- Two years: 40% discount

- Three years: 50% discount

- Four years: 60% discount

- Five+ years: 65-70% discount

That discount applies to your base premium, so it saves serious money.

A £2,000 policy with five years no claims? You’d pay around £600-700 instead.

Don’t claim for minor bumps.

If the damage costs less than your excess plus the no claims discount you’d lose, pay yourself.

Shop Around Every Year

Loyalty doesn’t pay in insurance. Your current insurer probably won’t offer their best price for renewal.

Start shopping 4 weeks before renewal.

Statistics from Go Compare show that renewing 26 days before your renewal date will get you the lowest price

Prices change daily, and you might find better deals with different timing.

Use comparison sites, but don’t stop there.

Some insurers don’t appear on them. Check Direct Line, Aviva, and Churchill’s websites directly.

Get quotes from specialist young driver insurers too:

- Admiral

- Hastings Direct

- Co-op Insurance

- Marmalade

Don’t just look at price. Check excess amounts, coverage limits, and customer reviews.

Increase Your Voluntary Excess

Your excess is what you pay before insurance kicks in.

Higher excess = lower premium.

But be smart about it.

Don’t set it higher than you can afford if something goes wrong.

If you can comfortably pay £500 in an emergency, increasing your excess from £200 to £500 might save £200+ on your premium.

Just remember – you’ll pay that excess for any claim, even if the accident wasn’t your fault.

This is where having an emergency fund can come in handy.

Take a Driving Course

Pass Plus isn’t the money-saver it used to be.

MoneySuperMarket research found the qualification made no difference to average driver premiums in 2024-2025.

Only a few insurers still offer discounts:

Adrian Flux: Up to 25% discount

Churchill: 5% discount

Diamond: Up to £250 discount for new drivers

Course costs range from £150-£250 generally, though Wales offers Pass Plus Cymru for just £20.

Advanced courses like IAM RoadSmart or ROSPA training might offer better value, with some insurers providing bigger discounts for these qualifications.

Secure Your Car Properly

Where you park and how you secure your car affects your premium significantly.

Here’s something surprising: driveway parking produces the lowest average premiums at £627, while locked garages cost £710 on average.

Street parking averages £729.

This happens because garages pose maneuvering risks and can signal to thieves which house contains car keys.

Security devices help too. Thatcham-approved tracking devices (S5 class) offer up to 20% premium reductions. Dash cams can provide up to 20% discounts from some insurers.

Many modern cars have immobilisers fitted as standard. Make sure your insurer knows about any security features.

Consider Multi-Car Policies

If your family has multiple cars, bundling them together often saves money.

Multi-car discounts apply to each additional vehicle beyond the first.

AXA offers up to 15% and Aviva provides 10% per additional vehicle.

Admiral’s MultiCar customers saved at least £378 according to recent data.

You’ll all need to be with the same insurer, and claims affect everyone’s no claims bonus. But the savings often make it worthwhile.

Policies typically cover up to 5 vehicles registered at the same address.

What Next?

The key to cheaper car insurance?

Start with trying a couple of these strategies and stick with them.

Your future self will thank you when you’re paying hundreds less each year.

Your insurance costs will naturally drop as you get older and build experience.

But why wait when you can start saving immediately?

If you found this interesting, please share!

Disclaimer: Content on this page is for informational purposes and does not constitute financial advice. Always do your own research before making a financially related decision.