A stocks and shares ISA lets you invest up to £20,000 a year with no UK tax to pay on your gains, dividends or interest.

It is one of the simplest ways to grow your money over the long term.

Here is how one works, what you can hold in it, and how to open one.

What is a stocks and shares ISA?

ISA stands for Individual Savings Account.

A stocks and shares ISA is one where your money is invested rather than left sitting as cash.

The big draw is tax.

Any growth, dividends or interest you earn inside it is free from income tax and capital gains tax, so there is nothing to declare and nothing to pay.

How does a stocks and shares ISA work?

You pay money in, up to £20,000 each tax year, and use it to buy investments like shares, funds and bonds.

Anything those investments earn stays tax free inside the ISA.

There are two main ways to run one:

Self-invested (DIY): you choose your own shares, funds and bonds.

Full control, but you are on your own unless you go looking for help. Better suited to people who know what they are after.

Ready-made (managed): the provider builds and runs a portfolio for you, based on how much risk you are comfortable with.

Fees are usually a little higher, but it is the easier place to start as a beginner. These are often called robo-advisors.

You can pay in as a lump sum or make ad-hoc payments whenever suits you.

Your money is covered up to £85,000 by the Financial Services Compensation Scheme if your provider goes bust.

Worth knowing: that protects you against the provider failing, not against your investments falling in value. Always check a provider’s fees before you commit.

Can You Hold Cash in a Stocks and Shares ISA?

Yes. Most providers let you keep some of your balance as cash, for example while you decide what to buy or after selling something. From April 2027, under rules confirmed in June 2026, interest earned on cash sitting in a stocks and shares ISA will face a 22% charge (still subject to consultation). It only hits cash interest, your actual investments (shares, funds, ETFs, bonds and gilts) are unaffected, and money market funds are exempt. The takeaway is simple: a stocks and shares ISA is for investing, so keep your money invested rather than parked as cash for long stretches. The £20,000 allowance and the way the ISA works are otherwise unchanged by the 2027 reforms.

How much can I pay into my stocks and shares ISA?

Your total ISA allowance is £20,000 per tax year, across every ISA you hold, whether that is cash, stocks and shares, or a mix.

Since April 2024 you can pay into more than one stocks and shares ISA in the same tax year if you want, as long as your total payments stay within that £20,000.

Not every provider allows it, so check first.

You can also split your allowance between a cash ISA and a stocks and shares ISA.

Any allowance you do not use is lost when the tax year ends on 5 April, so a lot of people top up before the deadline.

What about withdrawals?

You can usually take money out of a stocks and shares ISA whenever you want, though selling the investments and getting the cash can take a few days.

One catch: with most ISAs, money you withdraw and then pay back in counts towards your £20,000 allowance again.

Some providers offer a “flexible” ISA that lets you replace withdrawn money in the same tax year without it counting twice, which is worth checking if you think you might dip in.

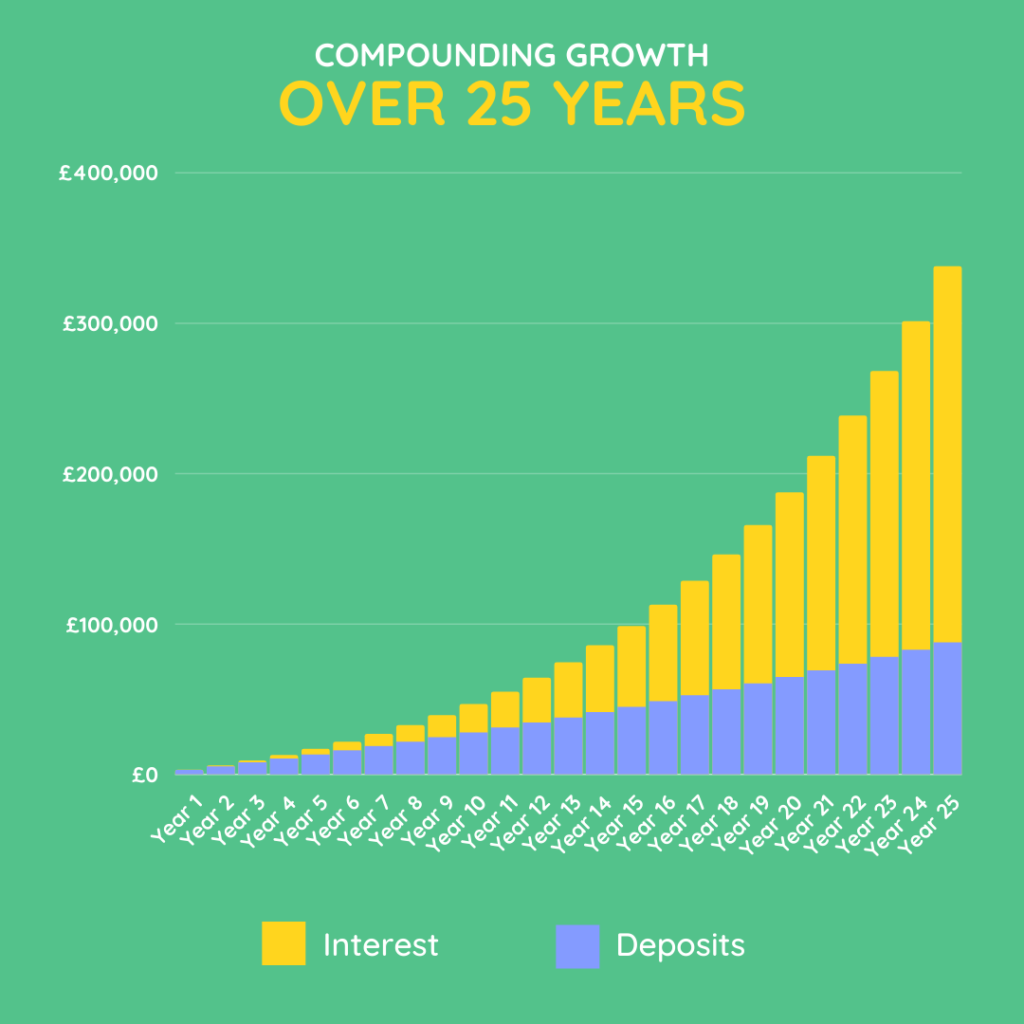

How much could I make?

The value of investments goes up and down, and you can get back less than you put in.

That is why a stocks and shares ISA suits money you can leave alone for at least five years.

Returns are never guaranteed.

But to show the effect of compounding, say you made a £20,000 investment and it grew by an average of 8% a year:

- After 20 years: around £93,000

- After 30 years: around £201,000

- After 40 years: around £435,000

Same £20,000, and the only extra ingredient is time. That is the power of compound growth.

What can you actually hold?

What you hold depends on the type of ISA you chose.

Self-invested (DIY): you pick everything yourself, from individual shares and funds to ETFs, bonds or investment trusts. You are in full control of exactly what your money buys.

Ready-made (managed): the provider builds a diversified portfolio for you, matched to the risk level you choose when you sign up. You decide how much risk to take, and they handle the picking.

Either way, most providers let you invest worldwide, including the big US “blue chip” names that anchor a lot of portfolios.

Prefer to avoid certain industries? Many providers offer an ethical or ESG option that screens out things like gambling, tobacco, fossil fuels and animal testing, and leans towards companies with stronger environmental and social records.

You can even get crypto exposure inside an ISA. Not the coins themselves, but funds and companies that hold them.

View our list of the best stocks and shares ISAs.

What happens to my ISA if I die?

ISAs do not simply vanish when you die. Your provider can either transfer the ISA to your spouse or civil partner, or sell the investments so the proceeds go into your estate.

A surviving spouse or civil partner can also inherit your ISA allowance on top of their own, which providers call an “additional permitted subscription”.

The executor of your will arranges all this, so it helps to leave a note of where your investments are held.

How to open a stocks and shares ISA?

Opening one is quick, usually through a provider’s app or website.

You will give basic details like your name, address and contact info, then answer a few questions about your experience and how much risk you are happy with, so they can point you to suitable options.

Before you pick a provider, do a bit of homework:

- Compare fees. You will usually pay a platform or account fee plus charges on the funds themselves.

- Look at past performance to get a feel for what to expect, though it is never a guarantee.

- Check the ethical options if sustainable investing matters to you.

A few providers worth a look, each offering a sign-up bonus for new customers:

- Trading 212

- IG

- Freetrade

Final Thoughts

A stocks and shares ISA can grow your money faster than a cash ISA over time, but your investment can also fall in value, so it is best treated as a five to ten year plus plan.

Leave it alone and let compounding do the work. For anything you might need sooner, keep a separate emergency fund in an easy-access savings account so you are never forced to dip into your ISA and eat into your allowance.

When you are ready, comparing a few providers is the best place to start.

Stocks and Shares ISA FAQs

Share this article with friends

Disclaimer: Content on this page is for informational purposes and does not constitute financial advice. Always do your own research before making a financially related decision.