The Lifetime ISA (LISA) is a versatile savings tool for UK residents aged 18-39, offering a unique blend of government bonuses and tax efficiency.

With a yearly limit of £4,000, savers receive a 25% government top-up, maximising their investment for either purchasing a first home or planning for retirement.

While the benefits are substantial, including tax-free growth, it’s crucial to be mindful of the conditions, such as withdrawal penalties for non-qualified expenses and the age limit for contributions and bonus eligibility.

Update (June 2026): the Lifetime ISA is being replaced. The Government has confirmed the Lifetime ISA will be replaced by a new First-Time Buyer ISA from April 2027 (still subject to consultation). For now nothing changes: the £4,000 annual limit and 25% government bonus both continue. The key thing to know is that the replacement is aimed at first-home buyers, so the Lifetime ISA’s use for retirement saving may not carry over in the same form. Separately, from April 2027 a 22% charge will apply to interest earned on cash held inside a Lifetime ISA. We will update this guide in full once the detailed rules are confirmed.

Have you recently been thinking about your finances? Maybe you have been figuring out where best to put your money.

You might have looked at a lifetime ISA, you might have even opened one and deposited some money.

But how does a lifetime ISA work? Let’s have a look!

Table of Contents

Get your FREE Money Action Plan

Take Our Quiz Now ?

Take Our Quiz Now ?

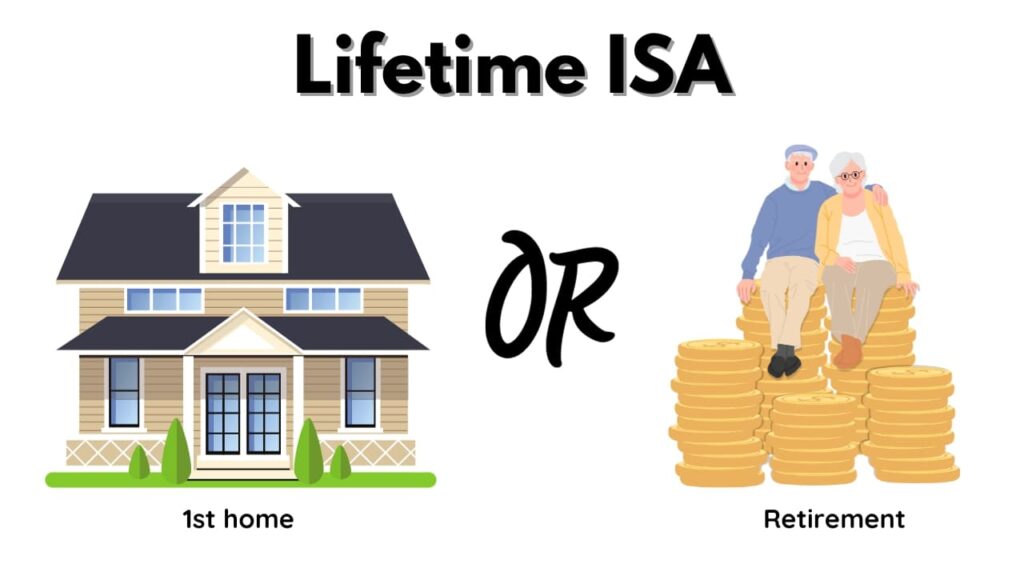

What is a LISA?

It’s a type of savings account to help you purchase your first home or help you towards retirement.

The money can be saved or invested depending on the type of LISA the provider offers. There are two main types a Cash or Stocks and Shares Lifetime ISA (more on this below).

The account must be open for a full 12 months from the day you open it to receive the bonus.

Open a Lifetime ISA in under 5 minutes with award-winning provider HL.

LISA age requirements

Firstly, we need to establish who can get a lifetime ISA, or LISA as it’s often referred to. In order to open a lifetime ISA, you need to be a UK resident between the ages of 18 and 39.

The earlier you open it, the more years you will have to pay into it and earn a bonus before the cut-off of the age of 50.

How does a Lifetime ISA work?

So how does a lifetime ISA work? The whole idea behind a lifetime ISA is to get you to either buy your first home or contribute to further retirement.

The current lifetime ISA rules are that you can pay a maximum of £4000 into the account each year.

The money you deposit will earn a bonus from the Government. That bonus is 25%.

So if you were to pay in the full amount in a year, you would get an extra £1000. Turning your £4k into £5k. The bonus is paid until you are 50. So if you were to deposit £4k every year from the age of 18, you could earn an additional £32k.

You can see how much this could add up to over the long term using our Lifetime ISA Calculator.

When you get to this point, you won’t be able to pay in any more money however you’ll earn interest and your account will stay open.

The maximum of £4k you can pay into a LISA each year is part of your overall 20k ISA allowance.

If you paid £4000 into your lifetime ISA, you’d still have £16k allowance to use for other ISA products such as cash ISAs, stocks and shares ISAs or innovative finance ISAs.

What are the tax benefits?

Saving your money in a tax-free way is great. This is what a lifetime ISA allows you to do. You can hold cash, stocks and shares or a combination of both in your LISA.

A lifetime ISA is a long-term savings account where you don’t pay tax on any interest or investments. You will not pay tax on the bonus either.

How is the bonus paid?

The 25% Government bonus is paid monthly.

It’s worth noting that the bonus is based only on money paid in. Not on investment growth or interest.

Depending on the provider you opened the account with, you’ll be able to keep an eye on your account via an app, online, over the phone or by visiting a branch.

Types of LISA

There are two main types of Lifetime ISA to be aware of. It’s vital to understand this distinction as each type differs in its purpose.

Cash Lifetime ISA

The Cash lifetime ISA follows the same principle as the Cash ISA where the money is saved like a standard savings account.

The difference being if you save inside the ISA then the withdrawal restrictions apply.

Stocks and Shares Lifetime ISA

When can I withdraw the money?

Withdrawing the money depends on your situation and what you are using the cash for.

Lifetime ISAs can be used to save for a first home. You can use your money towards buying your first property. LISAs are also used to save for retirement. You’ll be able to access the money if you are saving for retirement and are over the age of 60.

If you develop a terminal illness with less than 12 months to live, you will also be able to access the money in your lifetime ISA.

You’ll need written evidence from a UK-registered medical practitioner about your situation and any withdrawals will be exempt from charges.

Any withdraws away from these reasons will incur a 25% withdrawal charge.

If you were to die, your LISA closes on your day of death. The money and investments of your lifetime ISA will go to your beneficiaries. There are no charges to withdraw from the account.

Lifetime ISA for buying a house

If you are using a lifetime ISA to save money to put towards a house purchase, there are certain criteria you need to hit.

You have to be in the UK and the property you are buying has to be the first one you own. You also have to intend to live there and be buying with a mortgage. The property must have a price of £450,000 or less.

LISAs are individual, so if you are buying with someone else, they can also have a LISA, as long as they meet the eligibility. This would mean you can both put your bonuses towards the house purchase.

If you’re buying with someone who has owned a property before, they aren’t a first-time buyer, however, you can still put your bonus towards the purchase.

A lifetime ISA can be used to buy land for a self-build property. You just need to check that the purchase meets all the other criteria.

LISAs must have been open for at least 12 months in order to be eligible for the Government bonus.

House buying is often a dream for people, however, in reality, things can be much different. Sales can fall through. If this happened, your solicitor would be able to put the money and bonus back into a LISA for you to use at a later date.

Lifetime ISA for retirement

If you have one eye on your financial future, a LISA can be a great way to save for retirement.

From the age of 18, putting away £4k a year will give you a bonus of up to £1,000 a year until you are 50 years old. You’ll be able to access the money when you turn 60, making full or partial withdrawals without paying a fee.

It can be a great alternative to a workplace pension, for anyone who is self-employed or freelance.

32 years of putting £4k away would give you £128k, before the £32k bonus. That’s without taking into account interest or investment growth. A pot of money worth £160k+ could be a great way to enjoy retirement.

How does a Lifetime ISA differ to a Help To Buy ISA

The Lifetime ISA (LISA) and the Help to Buy ISA are both UK government schemes designed to help individuals save for their first home, but they have key differences:

Age Eligibility: LISAs are available to individuals aged 18-39, while the Help to Buy ISA was open to anyone over 16.

Government Bonus: Both offer a 25% government bonus, but LISAs have a higher annual contribution limit (£4,000) compared to the Help to Buy ISA (£2,400, or £3,400 in the first year).

Withdrawal Rules: LISA funds can be withdrawn tax-free if used for a first home purchase or after age 60. Withdrawals for other reasons incur a 25% penalty. In contrast, Help to Buy ISA funds could be withdrawn for a first home purchase without penalty, but other withdrawals would not receive the bonus and would have different interest conditions.

Contribution Limits: LISAs allow contributions and bonuses until age 50, while Help to Buy ISAs had lower contribution limits and a final deadline for contributions.

Property Price Limits: Both have property price limits, but they may vary by scheme and region.

Account Type: LISAs can hold cash or stocks and shares, offering more flexibility in investment choices compared to the cash-only Help to Buy ISA.

It’s important to note that the Help to Buy ISA scheme closed to new accounts on 30th November 2019, but existing accounts could keep paying in until November 2029, and the government bonus had to be claimed by 1 December 2030.

Get your FREE Money Action Plan

Take Our Quiz Now ?

Take Our Quiz Now ?

Lifetime ISA FAQs

At the June 2026 announcement the Government said the Lifetime ISA will be replaced by a First-Time Buyer ISA from April 2027. For now the £4,000 limit and 25% bonus continue, and we will update this guide once the detailed rules are confirmed.

25% on what you pay in, up to £1,000 a year on the £4,000 you can contribute. It is paid monthly and is based on your contributions, not on growth or interest.

Monthly, usually within a few weeks of your contribution reaching the provider. Your account must have been open at least 12 months before you can use it to buy a home.

In a cash LISA your balance will not fall, but a stocks and shares LISA can go up or down with the markets. The 25% withdrawal charge can also leave you with less than you put in.

A 25% government charge on the amount withdrawn for anything other than a first home, reaching age 60, or terminal illness. Because it is 25% of the larger, bonus-inflated amount, you can get back less than you paid in.

A cash LISA suits money you will need within about five years, such as a near-term house deposit. A stocks and shares LISA suits longer horizons like retirement. Both receive the 25% bonus.

Conclusion

If you have any friends asking the question of how does a lifetime ISA work, you’ll now be able to pass on the information.

LISAs can be a great way of saving for a house or for your future, however, you need to make sure you can afford to put this money away.

Withdrawing early can come with penalties and fees which can make saving not worth it in many situations. However, the Government bonus is a great way to top up your savings, so a lifetime ISA should be a serious consideration.

Share this article with friends

Disclaimer: Content on this page is for informational purposes and does not constitute financial advice. Always do your own research before making a financially related decision.