Most money advice sounds great on paper but falls apart when you actually try it.

You know the type – the stuff that assumes you’ve got a spare grand lying around or that you can just “stop buying coffee” and magically become wealthy.

But some rules? They’re actually worth paying attention to.

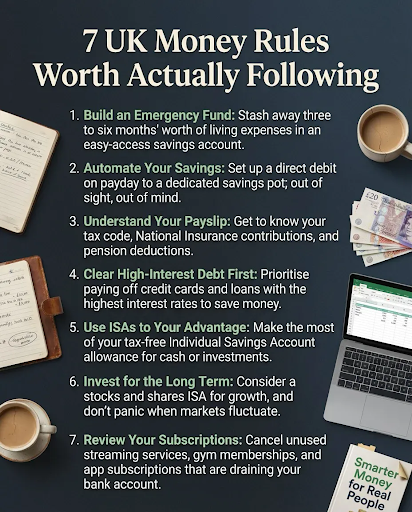

Build an Emergency Fund

This one gets thrown around a lot, but here’s the thing – it works.

You need three to six months’ worth of living expenses sat in an easy-access savings account. Not invested. Not locked away. Just sitting there, ready for when your car breaks down or your boiler packs in.

I know it sounds boring. And I know you’d rather use that money for literally anything else.

But the first time you avoid going into debt because your washing machine died, you’ll get it. That’s when this rule clicks.

Automate Your Savings

Want to know the easiest way to save money? Don’t give yourself the chance to spend it.

Set up a direct debit on payday to a dedicated savings pot. Out of sight, out of mind.

When the money never hits your current account, you can’t spend it on stuff you don’t actually need. Your brain adjusts faster than you’d think.

Start small if you need to. Even £50 a month adds up to £600 a year. That’s not nothing.

Understand Your Payslip

How well do you actually know your payslip?

I mean really know it – not just glance at the bottom line and move on.

Your tax code matters. Your National Insurance contributions add up. And those pension deductions? They’re building your future.

Take five minutes to properly understand where your money goes each month. You might spot errors. You might realize you’re paying too much tax.

Most people never bother. Be different.

Clear High-Interest Debt First

This one should be obvious, but here we are.

If you’ve got credit card debt at 20% APR and a car loan at 5%, which one should you pay off first?

The credit card. Every time.

High-interest debt costs you actual money every single day you carry it. Thousands of pounds over time, just vanishing into interest payments.

Clear the expensive debt first. It’s not sexy, but it saves you the most money.

Use ISAs to Your Advantage

ISAs are brilliant. Genuinely.

You can stash away £20,000 a year (as of 2026/27) and never pay a penny in tax on the interest or growth. Not now, not ever.

Whether you go for a Cash ISA or a Stocks and Shares ISA depends on your situation. But the tax-free bit? That’s the same for everyone.

Most people don’t max out their ISA allowance.

Most don’t even use it. If you’ve got money sitting in a regular savings account earning interest, you could be paying tax you don’t need to pay.

Invest for the Long Term

Here’s where people get nervous.

Investing isn’t just for rich people or City types. A Stocks and Shares ISA is available to anyone with a few quid to spare.

But – and this is important – you need to think long-term. Years, not months.

Markets go up and down. Sometimes they crash. If you panic when that happens and sell everything, you lock in your losses.

Stay invested. Ride it out. Over the long haul, stocks have historically beaten cash savings.

Can’t guarantee it, obviously. But history’s on your side.

(This post does not constitute financial or UK tax advice. Capital is at risk when you invest. Always do your own research)

Review Your Subscriptions

How many subscriptions are draining your bank account right now?

Netflix, Spotify, Disney+, that gym you haven’t been to since January, Amazon Prime, the Apple storage you forgot you had…

They add up faster than you think. £10 here, £15 there. Before you know it, you’re paying £100+ a month for stuff you barely use.

Cancel the ones you don’t actually need. Keep the ones you do. But at least know what you’re paying for.

You’d be surprised how many people have subscriptions they genuinely forgot existed.

And if you want the easy way to check, Gains App does this for you.

Why These Rules Matter

None of these are complicated.

You don’t need a finance degree. You don’t need to be earning six figures. You just need to pay attention to the basics.

Build a safety net. Automate good habits. Understand where your money goes. Kill expensive debt. Use tax-free accounts. Invest for the future. Stop paying for stuff you don’t use.

That’s it. That’s the list.

Will it make you rich overnight? No.

Will it put you in a significantly better position than most people? Absolutely.

The Part Nobody Talks About

Here’s what makes these rules actually work – consistency.

You can’t do them for three months, get bored, and expect results. Money management is a long game.

Emergency fund running low? Top it back up.

Cleared your credit card? Keep it clear.

Maxed your ISA? Do it again next year.

The people who do well with money aren’t the ones who earn the most. They’re the ones who stick to the boring stuff that works.

Start With One

If all of this feels overwhelming, just pick one rule and start there.

Maybe it’s setting up that direct debit for £50 a month. Maybe it’s finally checking your payslip properly. Maybe it’s cancelling three subscriptions you never use.

Just start somewhere.

You can add more as you go. But trying to overhaul your entire financial life in one go? That’s how people burn out and give up.

What About Everything Else?

These seven rules won’t solve every money problem you’ve got.

They won’t tell you how to negotiate a pay rise. They won’t explain buying a house. They won’t break down the pension system.

But they’ll give you a foundation. A solid base to build on.

And honestly? That’s more than most people have.

Do They Actually Work?

I wouldn’t be writing about them if they didn’t.

Emergency funds keep you out of debt. Automated savings actually get saved. Understanding your payslip can literally save you money.

ISAs are free money (in terms of avoiding tax). Investing beats inflation. And subscriptions? They’re just unnecessary drains on your account.

This isn’t theory. It’s what works in practice, for real people, in the UK, right now.

The Bottom Line

Financial advice doesn’t need to be complicated to be effective.

These seven rules are straightforward. They’re accessible. And they work whether you’re earning £20,000 or £200,000.

You just need to actually follow them.

Most people know this stuff already. The difference is doing it.

So what’s stopping you?

Share this article with friends

Disclaimer: Content on this page is for informational purposes and does not constitute financial advice. Always do your own research before making a financially related decision.