When you look at the house buying process from start to finish, it can all seem a little overwhelming.

That’s why I’ve put together this first time buyer guide, full of top tips to help with buying your first home.

I bought my first home in 2021 and it was THE most daunting thing I’ve ever done.

I knew basically nothing about what to do before getting into it and honestly I wish I had a guide like this that actually had some actionable tips!

Among other things, I’m going to be covering:

- How to find your perfect home

- What you need to know about mortgages and deposits

- Types of ownership

- Putting in an offer

- Contracts and exchanging on your home

- The fees when buying your first home

- How to make your house a home

The average age of a first-time buyer in the UK is now over 36 years old.

The positive aspect here is that, if you start soon enough, you’ve got plenty of time to get your finances in order and to start taking those first few steps.

Table of Contents

How To Buy Your First Home?

Buying your first home requires a few basics. 1st you need to actually find a house, then you need to have the deposit, a mortgage, and finally the legals.

In between there are lots of little naunces and first time buyer tips that you’ll need to know.

For me there isn’t a ‘best way to buy your first house’ you need to understand every situation will be different.

The process will stay the same but the length of time it takes to buy a house will differ hugely depending on what you’re buying, who you’re buying it from and how long the legals take!

Right now the markets are very volatile and mortgage rate rises are all over the news.

People are wondering whether it’s worth buying a house or whether to stay put but for me, getting on the property ladder and owning your first home is an amazing achievement if your finances permit you to do so.

Key Takeaways

-

Start Saving and Check Your Finances: Begin saving for your deposit as early as possible, aiming for at least a 5-10% deposit. Ensure your credit score is in good shape and understand all the associated costs of buying a home, including stamp duty, legal fees, and mortgage arrangement fees.

-

Explore Government Schemes and Get Mortgage Pre-Approval: Look into government schemes and accounts like a Lifetime ISA that could make buying more affordable. Secure a mortgage in principle to clarify what you can afford and strengthen your position as a buyer.

-

Research Locations and Think Long-Term: Investigate potential areas thoroughly, considering local amenities, transport links, and future developments. Choose a property that can accommodate your needs for the foreseeable future.

-

Negotiate and Get a Property Survey: Don’t hesitate to negotiate on price, and invest in a comprehensive property survey to uncover any potential issues before finalising your purchase.

-

Seek Professional Advice and Understand the Process: Consult with a financial adviser or mortgage broker to guide you through the complex home buying process in the UK, and be prepared for potential delays. Always plan for the future, considering the property’s resale value and potential for appreciation.

First Time Buyer Checklist

Based on my own personal experience here is my first time buyer checklist which I wrote out after we got our keys.

You can come back to this at any point but below we’re going to go into more detail on each point for you.

- Assess Your Financial Readiness: Ensure you have enough savings for a deposit and evaluate your credit score.

- Calculate Your Budget: Determine how much you can afford to spend, considering all associated costs.

- Explore Mortgage Options: Research different mortgage types and rates to find the best option for you.

- Get a Mortgage Agreement in Principle: Secure a provisional mortgage offer to strengthen your buying position.

- Research Government Schemes: Investigate if you are eligible for any government schemes.

- Choose a Reliable Estate Agent: Find an estate agent who understands your needs and has a good track record or go online.

- Identify Potential Properties: Start your property search based on your budget, preferred locations, and essential criteria.

- Arrange Property Viewings: Schedule visits to potential properties to get a feel for them in person.

- Make a Well-Informed Offer: Once you’ve found your ideal property, make a realistic offer based on market conditions and any identified issues.

- Hire a Solicitor or Conveyancer: Choose a reputable professional to handle the legal aspects of the purchase.

- Secure a Formal Mortgage Offer: Finalise your mortgage application and await approval from the lender.

- Commission a Property Survey: Have a professional survey conducted to identify any structural issues or necessary repairs.

- Finalise the Legal Work: Work with your solicitor or conveyancer to complete all necessary legal documentation.

- Prepare for Additional Costs: Ensure you have funds set aside for stamp duty, legal fees, and any other additional costs.

- Exchange Contracts: Once everything is in order, sign and exchange contracts with the seller, making the deal legally binding.

- Finalise Your Mortgage: Confirm the details of your mortgage and ensure all funds are in place for completion.

- Complete the Purchase: Finalise the transaction and take ownership of your new home.

- Move In: Organise your belongings and move into your first home.

- Set Up Your Utilities and Council Tax: Ensure all essential services are connected and council tax is set up in your name.

- Review Your Mortgage Regularly: Keep an eye on your mortgage deal and consider remortgaging if a better deal becomes available.

What websites are best to help with buying your first home?

It was once the case that when you were looking to buy a house you’d take a wander into your local town and spend hours staring into the windows of estate agents.

While estate agents still display properties in their windows, this is not always the best way to find your perfect home.

For one thing, it is hardly an efficient use of your time and, for another, you’re not going to find every available property being displayed.

The solution? Go online, and there’s really only two options worth considering.

Rightmove

This is perhaps the best-known property portal. It has been the most popular for many years now and you’ll find that there is practically every estate agent listed here.

On Rightmove, there is a great search function that makes it easy to find properties that are right for you. You can search by area, price, number of bedrooms, etc and really zone in on what’s right for you.

Another useful feature is the fact that you can look at how much houses have sold for recently. We’ll come onto this later, but this can provide a great guide when it comes to putting an offer in.

Zoopla

Arriving on the scene some seven years after Rightmove, Zoopla is hot on its heels and is the second biggest property portal in the UK.

Estate agents are attracted to Zoopla as it allows them to list their properties a bit cheaper than Rightmove does. That being said, Rightmove still has the biggest number of properties listed.

Getting your finances in order

This step should perhaps come first before you even start to look at potential homes.

There is no escaping the fact that you’re going to need to have your finances in order.

Unless you have managed to save significant funds, have inherited money or a house, or have been gifted one, the chances are that you’re going to need a mortgage.

A mortgage put simply, is just a loan that is used to buy a house. Perhaps unsurprisingly, these loans tend to be on the large side!

This means that before anyone is going to lend to you, you’re going to need to show that you’re able to keep up with the repayments.

How do you do this?

By looking after your credit file.

Your credit file gives lenders an overview of how you manage your finances. It shows the level of debt that you have and how you’re managing that debt. Missed and late payments are red flags and will put a mortgage company off.

It’s still possible to get a mortgage with a less-than-perfect credit file. The problem is that lenders will look for a bigger deposit and will also charge you a higher interest rate.

By staying on top of your finances, and managing your debt well, you’ll be given access to the best deals out there.

Some basic tips to help with your credit include:

- Check your credit report regularly

- Challenge anything on there that looks wrong

- Ensure you make all of your payments on time

- Use credit cards little and often. By always paying off your balance in full you’re showing you’re financially responsible

- Never use more than 50% of the credit you have available to you – the lower the percentage the better

- Resist the urge to make lots of credit applications in a short space of time

How much can I borrow?

If you’re looking into the dos and don’ts of buying your first house, one of the biggest ‘dos’ is to find out how much you can borrow.

Ideally, you should be exploring this before you even start to search for properties. After all, there’s little point in finding your perfect home only to discover later that it’s just not affordable.

So, how do you find out how much you can borrow? You’ll need to ask! Here’s a look at the ways that you can do that.

Approach lenders directly

Perhaps someone has recommended a lender where they’ve had a great experience. Maybe you have a good relationship with your bank and you want to start there.

There’s certainly nothing wrong with this approach, however, you may be limiting yourself to the mortgage products that are available and missing out on some of the best deals.

It’s important to have a list of questions to ask your mortgage advisor, so you get the best deal.

Speak to a mortgage broker

With this option, be sure that you find a broker who has access to the whole of the market. This means that you will be able to explore the best deals out there.

One of the first fees when buying your first home may well be made here as some brokers will charge for their advice.

These fees are usually worthwhile given the great deals that a mortgage broker can find.

Go online

Perhaps the thought of walking into offices or picking up a phone is a little too much. If so, you can still get all of the information that you need by exploring online brokers.

Companies such as onlinemortgageadvisor.co.uk have access to some of the best deals on the market and can save you a great deal of time.

Once you have looked at the deals on offer and found one that works for you, you can ask for a mortgage in principle (MIP).

This doesn’t involve a credit check but does show what a lender may be prepared to offer you in terms of a mortgage.

This means that you then know the prices of houses that you can start looking at. A MIP doesn’t 100% guarantee you a mortgage, but it does give you a good idea of what you may have access to.

Approval will be subject to a credit check and you provide various documents and information when requested.

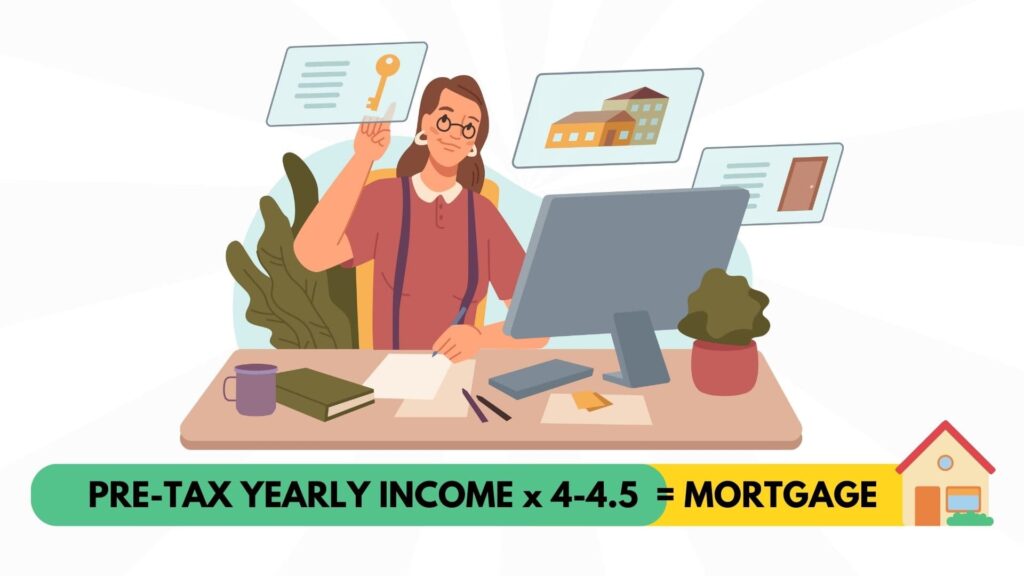

How is the mortgage calculated?

Understanding how the mortgage is calculated is quite simple. The amount that you will be able to borrow is based on affordability. Usually, you will be offered a multiple of your annual income which is around 4-5 times.

If there’s two of you on the application then that doubles.

However, there will also be consideration given to other payments that you need to make on a monthly basis. These amounts will be deducted so that the lender can calculate what is affordable for you.

Boon Brokers are one of the UKs leading online mortgage brokers. They have a 5-star excellent Trustpilot rating with over 543 reviews.

- No mortgage fees

- Whole of market access

- Free online consultations

- Directly authorised by the FCA

- No in person meet ups

Saving for a deposit

Tips to help with buying your first home have to include the fact that you need to save as much as possible towards your deposit!

While there are mortgages that allow you to borrow up to 95% of a property’s value, generally, the bigger the deposit you have the better deal you’ll get and the lower your monthly payments will be.

The best approach to a mortgage deposit is to start saving and investing as early as possible. If you make plans in your early 20s, by the time you reach the age of the average first-time buyer, you will find yourself in a great position.

If you’re like a large portion of the population that find it difficult to save money then check out our 10 tips here.

One option if you have it already is a Help to Buy ISA. The only thing is they stopped new accounts in 2019 so you’re only other option is a Lifetime ISA.

A lifetime ISA is a great option for saving.

When people look into these, they often wonder about the lifetime ISA purchase limit and want to know the answer to “How is the lifetime ISA bonus paid?”. Let’s explore lifetime ISAs a little more:

The Lifetime ISA

Released in 2017, a lifetime ISA provides a great way to save towards your mortgage deposit. If you are looking to buy your first property with a partner, you can both invest in separate lifetime ISAs and take full advantage of what’s on offer.

What’s great about a lifetime ISA is that the government will pay you a nice little bonus.

For every £250 that you invest, it will add an extra £50 (up to a maximum of £3,000). You are able to invest a maximum of £4,000 each tax year and, as you can imagine, this soon builds up.

Where do I get a lifetime ISA?

There are numerous banks and other financial institutions that offer lifetime ISAs. When it comes to choosing where to open yours, it is worth exploring track records to see how well institutions have performed.

The money in your ISA could be invested by whoever is running it with the hope of its value increasing. You need confidence that yours are in the best hands.

Two companies at the forefront of lifetime ISAs, and offering great returns, are Nutmeg and Fidelity.

Both companies offer you a hands-off approach to investing they take care of your funds so that you can concentrate on the other important things in life.

What fees will I pay when buying my first home?

It’s not just your deposit that you’ll need to save for when looking at buying your first house. Some of the others that you’ll need to factor in include:

• Lenders fees – these include a non-refundable booking fee, an arrangement fee, a survey fee to value the property, and transfer fees to send the funds that you’ve borrowed over to your solicitor

• Solicitor’s fees – a solicitor handles all the legal aspects of buying a house and, of course, they need paying for their services

• Stamp duty – a tax that you pay when you buy a property. How much you pay depends on the value of your property.

Usually, you start to pay if the property is worth more than £125,000. However, for first-time buyers, this limit is raised and so you won’t pay stamp duty on property worth up to £300,000.

Boon Brokers are one of the UKs leading online mortgage brokers. They have a 5-star excellent Trustpilot rating with over 543 reviews.

- No mortgage fees

- Whole of market access

- Free online consultations

- Directly authorised by the FCA

- No in person meet ups

Getting help buying your first home

Even if you have set about things in the right way, and begun to save at an early stage, it can still be challenging to get onto the property ladder.

House prices have outpaced wages for years, which is why the government runs schemes to give first-time buyers a leg up.

Most of the well-known ones from the 2010s have now closed – Help to Buy Equity Loan stopped accepting applications in October 2022 and the Help to Buy ISA closed to new accounts in 2019 – but there are still a few solid options on the table in 2026.

Here are the schemes still open to first-time buyers right now:

Lifetime ISA (LISA)

The single best government-backed account for most first-time buyers.

You can pay in up to £4,000 a year and the government adds a 25% bonus – that’s up to £1,000 free, every year, until you turn 50.

The money has to go towards a first home worth £450,000 or less, or it’s locked away until age 60 (with a 25% withdrawal penalty if you take it out for anything else).

If you and a partner are both saving, that’s £2,000 a year between you in free money.

We’ve got a full guide to the Lifetime ISA if you want the full breakdown.

First Homes Scheme

A government-backed discount scheme for new-build properties in England.

Eligible first-time buyers can buy a designated home for 30% to 50% below market value, with the discount baked into the property’s title – so when you sell, the next buyer gets the same discount.

There’s a household income cap (£80,000, or £90,000 in London) and a price ceiling on the discounted home (£250,000, or £420,000 in London).

Availability varies by local authority. Check what’s live near you on the Own Your Home portal.

Shared Ownership

Instead of buying the whole property, you buy a share – typically between 25% and 75% – and pay subsidised rent on the rest.

Over time you can “staircase” up by buying more of the property.

It’s particularly useful if you can scrape together a deposit on a 25% share but couldn’t get a mortgage on the full price.

The trade-off: you’re a leaseholder, there are service charges, and selling can be slower because the housing association usually has the right to find a buyer first.

Stamp Duty First-Time Buyer Relief

Not a “scheme” exactly – it’s a built-in tax break.

As a first-time buyer in England or Northern Ireland you pay no Stamp Duty Land Tax on the first £300,000 of a property, and a reduced rate up to £500,000. (Above £500,000 you pay the standard rates with no relief at all.)

The thresholds reverted on 1 April 2025 from the temporarily higher levels that ran from 2022 to 2025, so this is the current setup as of the 2026/27 tax year.

Scotland (LBTT) and Wales (LTT) have their own thresholds and reliefs — check the gov.uk page for your nation if you’re not buying in England or NI.

95% Mortgages

These are now part of the standard high-street mortgage menu rather than a separate “scheme”.

Most major lenders offer 5% deposit products, and you’ll find them through any whole-of-market mortgage broker.

Worth a conversation with a broker to see what your borrowing power actually looks like – see our mortgage calculator for a quick estimate first.

Part ownership vs full ownership

One of the tips to help with buying your first home is to explore the possibility of part ownership. Why would you want to do this?

Well, if you only own part of the property, it may be easier to raise the deposit that you need to go ahead and take out a mortgage.

With full ownership, you own the property as a whole. This means that you have full responsibility for its upkeep, but you’re free to do whatever you’d like in terms of decorating and alterations (with the exception of structural changes that may require planning permission).

Part ownership works a little differently.

You buy just a percentage of the property while a housing association owns the rest. This option still requires a mortgage for part ownership but you also pay rent to the housing association for the proportion of the property that it owns.

This means that you are making a mortgage payment and a rent payment each month. As you don’t own the property, there may be restrictions placed on any changes that you can be made.

While part ownership offers a cheaper way to get onto the property ladder, there are certain drawbacks such as:

- Not all lenders will offer mortgages for this type of setup

- It’s not always easy to sell your share if you want to move

- You will have to pay fees for maintenance

- The property will be leasehold rather than freehold

Not everyone is aware of the differences between leasehold and freehold, so that’s what we’ll be exploring next.

Freehold vs leasehold

When you opt for a freehold property, you’re getting the whole package: the house and the land it’s on. It’s completely yours.

On the flip side, with a leasehold, it’s a bit like renting the place for a very long time, typically around 120 years, though it can vary from 40 to 999 years.

Most people tend to prefer freehold. That’s because, even though leasehold might be cheaper to start with, it comes with its own challenges.

You’re not the full owner of the property, and on top of your mortgage, there are extra fees like ground rent and service charges.

Plus, if you want to make any major changes, you need the green light from the freeholder.

And when it’s time to sell, leasehold properties can be trickier to pass on since most buyers are after the full ownership deal.

With freehold, you have more control, but it might hit your wallet a bit harder upfront. Leasehold might be kinder on your budget initially, but those extra fees and the reduced freedom are important to weigh up.

Making an offer

Looking into the dos and don’ts of buying your first house, it is important not to rush in when it comes to making an offer on a home.

Just because a house is advertised at a certain price, that doesn’t mean that is what you’re going to need to pay.

A lot depends upon how the property market is. Right now, we are in a seller’s market so you may well need to offer the asking price straight away.

However, markets change and there are then opportunities to offer much less than what is being asked for.

Some of the steps that you should take before putting in an offer include:

- Researching the area that you’re looking at

- Using Rightmove and Zoopla to look at previous house prices

- Find out how long the property has been on the market for

- Be sure that you know how much you can borrow

If the seller accepts your offer, you need to ask for it to be taken off the market.

While your offer is not legally binding you don’t want to risk someone else coming along and offering more and you losing out.

As soon as this happens, it’s time to get the ball rolling and get your mortgage ready to go

Mortgage application stages

So, you’ve found your perfect first home and the seller has accepted your offer.

What do you need to do next to make sure that you can pay for the house?

You’re going to have to put in your final mortgage application.

Hopefully, you already have a mortgage in principle, so now is the time to give the lender the full details that it needs to get the money across to you.

Some of the documents that the lender will want to see include:

- Prove of who you are such as a driving licence or passport

- A bank statement, utility bill, or council tax bill to prove your current address

- Proof that you have the deposit taken care of

- After the mortgage has been provided you’ll also need to prove that you have buildings insurance in place

Once the lender has all of the documents that it needs, it will go ahead and carry out both credit and affordability checks.

The lender will also want to get the house valued so that it can be sure that you’re not paying more than it’s worth.

Should you fail to keep up your payments, the house is the lender’s security and it needs to know that it can recover its money if it comes to it.

Waiting for your mortgage to be approved can be a tense time. It’s common for the process for a mortgage to take 3-6 weeks and this can feel like a lifetime of waiting!

Boon Brokers are one of the UKs leading online mortgage brokers. They have a 5-star excellent Trustpilot rating with over 543 reviews.

- No mortgage fees

- Whole of market access

- Free online consultations

- Directly authorised by the FCA

- No in person meet ups

The conveyancing process

Not everything sits still while you are waiting to hear about your mortgage. At the same time, your solicitor will be getting to work and carrying out searches on your property. These searches include:

Local authority searches.

These searches are carried out to spot potential issues such as:

- Building control

- Rules around a conservation area

- Road schemes

- Enforcement action

Exciting right? Well, this looks at whether the house is at risk of flood or damp issues. It also confirms that the property is connected to the sewers and establishes how water is provided and paid for.

Of course, your house won’t always have been standing! These searches look at what the land was used for in the past and can highlight issues such as potential contamination.

While it is not a requirement, this is the perfect time to book in a RICS surveyor. Rather than looking at the value of the property, they will be inspecting it to find any potential issues. Anything that you need to know about will be given to you in the form of a report.

How to exchange contracts?

Now we get to the exciting part! With your mortgage approved, the searches back, and your RICS report all good, it’s time to exchange contracts and agree on when you’re going to complete!

Exchanging contracts means just that. Both you and the seller sign copies and you swap these. You both end up with a signed copy. However, you don’t get the keys just yet!

Before you can move in, you’re going to need to pay for the house! This is done via your solicitor who will transfer the funds on your behalf.

You’ll also need to sign a deed of transfer and make sure that you pay your solicitor.

You get the keys and move in when you complete. This is typically a week or so after you’ve exchanged contracts but can be longer is some cases for example, if you’re waiting for the seller to complete on their home, known as a chain.

Completion day is when it’s all done and dusted and you officially become the owner of your first house. Now, you need to turn this house into a home!

Making your house a home

What’s really exciting about buying your first house is when you get the chance to make it your own.

How you decorate and your choice of furniture can say a lot about you and can really make your living space as unique as you are.

Of course, having paid a deposit and other fees along the way, funds may be a little tight when you first move in.

That’s why many first-time buyers explore shops such as Ikea for furnishing their homes. Why Ikea over other stores?

Well, Ikea has a great reputation when it comes to quality and it also offers some great storage solutions. Some of the must-buys include the likes of:

- A stylish wardrobe

- Garden furniture so that you can enjoy your outdoor space too

Getting the right furniture really adds the finishing touches to a house and makes it a home.

Share on social media

Disclaimer: Content on this page is for informational purposes and does not constitute financial advice. Always do your own research before making a financially related decision.