Here’s something most people get wrong about saving money: they think they need to completely change their lifestyle.

Cut out everything fun.

Stop buying coffee.

Never go out.

Live like a monk.

That’s rubbish. And it doesn’t work.

The easiest way to save money is to spend less on the stuff you’re already buying. Not to stop buying it. Just to pay less for it.

Let me show you how.

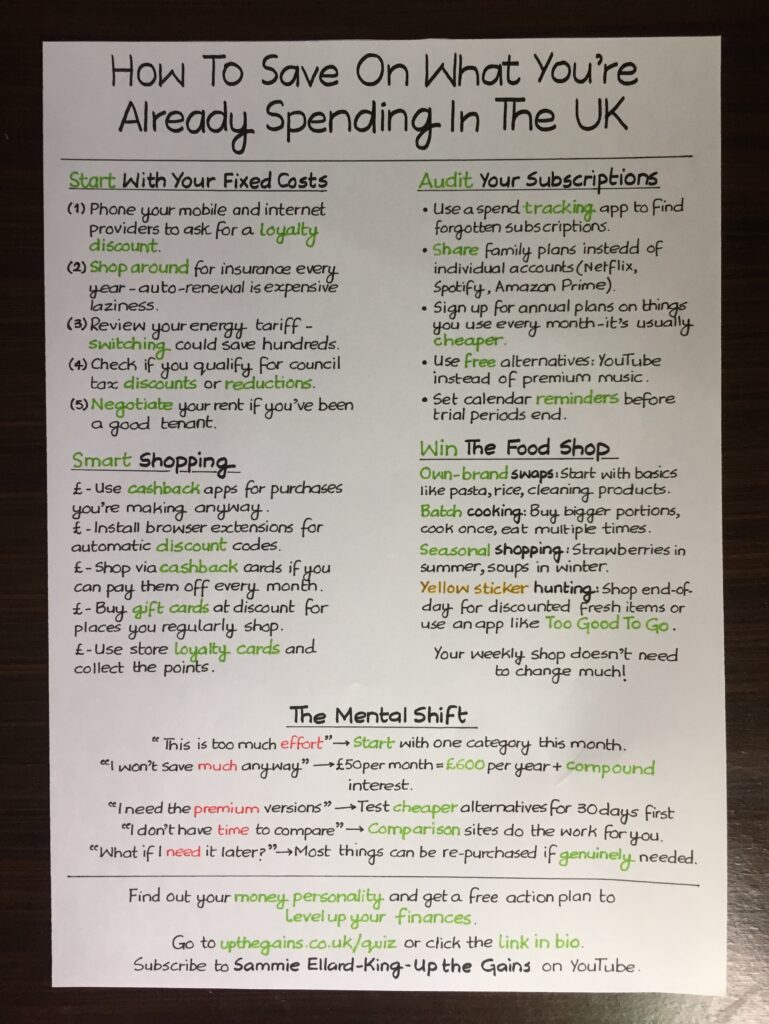

Your Fixed Costs Aren't Actually Fixed

The bills you pay every month don’t have to be fixed.

Turns out most of them can be negotiated with a little bit of planning and effort.

1) Phone Your Providers

When was the last time you called your mobile or broadband provider and asked for a better deal?

Most people never do this. They just accept whatever they’re charged.

That’s exactly what the companies want.

Here’s what you do: call them up.

Say you’re thinking of leaving because you’ve seen better deals elsewhere.

Ask what they can offer you to stay.

This works for mobile, internet and TV packages.

You’ll be amazed what discounts suddenly appear when you threaten to leave.

I’m talking £10-20 per month saved or more.

That’s £120-240+ per year from one phone call.

2) Insurance Costs Skyrocket If You Auto-Renew

Auto-renewal on insurance is expensive laziness. Your insurer is counting on you not bothering to shop around.

They bump your price up every year.

Not because the service got better. Because they can.

Set a calendar reminder one month before your renewal date. Use comparison sites to find a better deal.

Then either switch or use the quote to negotiate with your current provider.

This works for car insurance, home insurance, pet insurance, everything.

People save hundreds per year doing this. All for 30 minutes of work.

3) Energy Tariffs Change All The Time

If you’re on your supplier’s standard variable tariff, you’re probably paying too much.

Fixed tariffs often work out cheaper.

But you need to actually compare them.

Use sites like Money Saving Expert or Compare The Market.

See what’s available and switch if it makes sense.

This could save you £200-300 per year.

Maybe more depending on your usage.

4) Council Tax Discounts

Are you a single person? You get a 25% discount.

Are you a student? You might pay nothing.

Does someone in your house have a disability? There are reductions available.

Most people don’t claim what they’re entitled to.

The council won’t tell you up front. You have to ask and make the right applications but it’s so worth it.

5) Negotiate Your Rent

This one feels scary.

But if you’ve been a good tenant, it’s worth trying.

Especially if you’ve been there a while. Landlords don’t want the hassle and cost of finding new tenants especially with the risk of a bad tenant coming in next.

Send a polite message. Mention you’ve been reliable with payments. Ask if there’s any flexibility on the rent.

Worst case? They say no.

Best case? You could save £50-100 per month.

That’s £600-1,200 per year.

Your Subscriptions Are Bleeding You Dry

Most people have no idea what subscriptions they’re actually paying for.

Netflix. Spotify. Amazon Prime. Disney+. All costs adding up to do a lot of the same thing.

Maybe it’s a meditation app you used once or a gym membership you signed up for on a whim and never used.

This is how you can cut your subscription costs.

1) Find The Forgotten Ones

The easiest way is to use a spend tracking app like Gains that will show you every recurring payment.

You’ll probably find 3-5 subscriptions you completely forgot about.

Cancel them immediately.

That’s probably £20-40+ per month back in your pocket. Just like that.

2) Share Family Plans

Why are you paying for individual Netflix when you could split a family plan with mates?

Same with Spotify. Same with Amazon Prime.

Same with most streaming services.

Family plans cost a bit more than individual ones, but split between 4-5 people?

Everyone saves money.

3) Annual Plans Are Cheaper

If you use something every month and you know you will for the long run, pay annually.

Most services give you 2-3 months free if you pay for the year upfront.

That’s a 15-20% discount.

Obviously only do this for things you definitely use.

Don’t pay a year for something you might have wanted to cancel in two months.

4) Use Free Alternatives

Do you actually need Spotify Premium? The free version or YouTube works fine for most people.

Do you need that paid meditation app? There are loads of free ones.

Do you need premium LinkedIn? Probably not.

Question every subscription. Is the paid version genuinely adding value to your life? Or are you just too lazy to cancel it?

Once you have trimmed your spending, top it up with free wins: you can bag free stuff on your birthday from loads of UK brands.

5) Set Reminders For Trials

Free trials are brilliant.

Until they turn into paid subscriptions you forgot about.

Set a calendar reminder for two days before the trial ends.

Cancel it if you don’t want to pay.

Simple, effective and saves money.

Shopping Smarter Isn't Complicated

You’re going to spend money anyway.

You might as well get some of it back.

1) Cashback Apps Are Free Money

Cashback Apps give you money back on purchases you’re making anyway

If you’re shopping online you’ll want to check sites like TopCashback and Quidco first to check if they offer cashback.

For your everyday spending you need an instant giftcard cashback app like Gains.

Food shopping? Get cashback.

Booking a holiday? Get cashback.

Buying clothes? Get cashback.

It’s not a huge amount each time.

But it’s literally free money for less than a minute’s work before you shop and it could be hundreds of pounds a year back in your pocket.

2) Browser Extensions Do The Work

Install Honey or Pouch.

They automatically find discount codes when you’re checking out online.

You don’t have to search for codes. You don’t have to try 15 different ones. The extension does it.

Sometimes you save nothing. Sometimes you save 20%. Either way, it costs you zero effort.

And if you travel by train, grab a railcard. They knock a third off most fares for £35 a year.

3) Cashback Credit Cards

If you can pay off your credit card in full every month, consider a cashback credit card.

American Express, Barclaycard, and others offer 0.5-1% cashback on everything you spend.

Spend £1,000 per month? That’s £60-120 per year back. Just for using a different card.

Only do this if you pay it off in full.

Interest charges will wipe out any cashback benefit.

4) Use Loyalty Cards

Tesco Clubcard.

Nectar.

Boots Advantage.

Costa Coffee.

Whatever.

Just use them.

The points add up. You might as well get something back.

People who ignore loyalty schemes are leaving money on the table for no reason.

Watch this episode of The Money Gains Podcast with Chloe from Chloe’s Deals Club to learn more tricks to get money off your shopping.

Win The Food Shop

Food is probably your biggest variable expense.

Small changes here make big differences.

1) Own-Brand Swaps

Start with basics.

Pasta, rice, tinned tomatoes, cleaning products.

The Tesco Value pasta tastes exactly the same as the fancy brand.

It’s literally just pasta.

You don’t need to swap everything. Just the basics where there’s genuinely no difference.

Most people save £20-40 per month doing this.

That’s £240-480 per year.

2) Batch Cooking Saves Money

Buy bigger portions of meat or vegetables. Cook once to eat multiple times.

A whole chicken costs £5. That’s 3-4 meals if you’re smart about it.

Batch cook pasta sauces, curry and soup then freeze portions.

It’s cheaper than buying meal-deal sized portions every time and it’s way cheaper than takeaways.

3) Shop Seasonally

Strawberries in December cost a fortune because they’re imported.

Strawberries in June are cheap because they’re local.

Soup vegetables in winter are cheap. Salad stuff in summer is cheap.

Buy what’s in season.

It’s cheaper and it tastes better anyway.

4) Yellow Sticker Hunting

Shop at the end of the day. Look for yellow stickers on fresh items about to expire.

Bread, meat, vegetables, ready meals. All massively reduced.

Freeze what you don’t need immediately. You’ve just saved 50-75% on food that’s perfectly fine.

Apps like Too Good To Go let you buy end-of-day food from restaurants and shops for a fraction of the price.

Your weekly shop doesn’t need to change much.

You’re just paying less for the same stuff.

The Mental Blocks Holding You Back

Every time I suggest these things, people make excuses.

Let’s deal with some of them.

"This Is Too Much Effort"

You don’t have to do everything at once.

Start with one thing this month. Cancel unused subscriptions.

Next month, do another thing. Switch your energy bills.

Small changes compound.

You don’t need to overhaul your entire life in one day.

"I Won't Save Much Anyway"

£50 per month is £600 per year.

Put that in an investment account earning 8% and in 10 years you’ve got £9,200.

Still think it’s not worth it?

Small amounts add up. Especially when you invest.

"I Need The Premium Versions"

Maybe. But probably not.

Test cheaper alternatives for 30 days. If you genuinely miss the premium version, switch back.

Most of the time, you won’t notice the difference. You’re just used to paying more.

"I Don't Have Time To Compare"

Comparison sites do the work for you. You put in your details once. They show you all the options.

It takes 10 minutes for insurance. It takes 5 minutes for energy. It takes 2 minutes for mobile contracts.

If you can’t find 10 minutes to save £200, that’s a priority problem, not a time problem.

Do you earn over £1,000 an hour from your job? Probably not.

"What If I Need It Later?"

If you cancel a subscription and genuinely need it later, you can resubscribe.

If you switch to own-brand pasta and hate it, buy the branded one next time.

Nothing is permanent.

You’re not making life-or-death decisions here.

Start With One Thing

Don’t try to implement all of this at once. That’s overwhelming.

Pick one thing from this list and do it this week.

Maybe it’s calling your mobile provider. Maybe it’s cancelling forgotten subscriptions. Maybe it’s switching to own-brand basics.

Next month, pick another thing. Then another. Then another.

By the end of the year, you’ve made 12 changes.

You’re probably saving £100-200 per month. That’s £1,200-2,400 per year.

For what? For making a few phone calls and clicking a few buttons?

That’s the easiest money you’ll ever save.

Every pound you’re overpaying on bills is a pound that could be in your savings account.

Or your investment account.

Or your holiday fund.

Companies are betting that you won’t bother to check. That you won’t bother to compare. That you’ll just keep paying whatever they charge.

Most people do exactly that.

Don’t be most people.

It’s your money and your choice. Make it count.