Barista FIRE is the semi-retirement approach where you save enough that the 4% rule covers most of your annual expenses, and you cover the gap with low-stress part-time work.

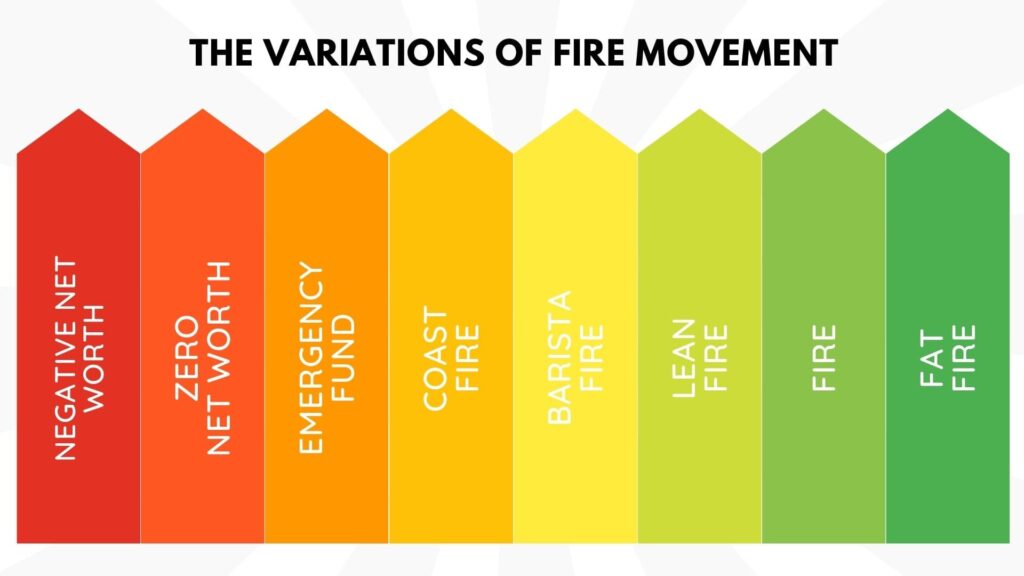

It sits between Lean FIRE (full retirement, frugal lifestyle) and Fat FIRE (full retirement, comfortable lifestyle), and it’s the version of FIRE most people I talk to in the UK actually find realistic.

Quick snapshot:

Your Barista FIRE number = (annual expenses ? part-time income) × 25

Example (UK): £30k annual spend minus £10k from part-time work = £20k gap. £20k × 25 = £500,000 invested. That’s roughly 40% less than traditional FIRE on the same lifestyle.

Typical UK setup: Stocks and Shares ISA + SIPP, drawing from the ISA before age 55, then SIPP on top from 55 (57 from 2028) onwards

The trade-off: You work part-time instead of stopping completely. Most Barista FIRE adherents say this is actually a feature rather than a cost

If you want to skip straight to the maths for your own numbers, use the Barista FIRE Calculator.

If you want to understand how it fits UK tax wrappers, keep reading.

Table of Contents

What is Barista FIRE?

The name comes from Starbucks. In the US, Starbucks offers health insurance to staff working as few as 20 hours a week, which made part-time coffee shop work a realistic way to bridge a full-time career and full retirement. Some of the earliest people to plan around this literally did become baristas. The name stuck, even though the health insurance angle barely matters here.

In the UK, the NHS makes that part of the story irrelevant. You don’t need a part-time employer for healthcare, which is arguably why Barista FIRE suits UK savers even better than the Americans who coined it.

Day to day, it looks like this: you leave your main career and pick up something lower-pressure two or three days a week, tutoring, freelance work in your old field, hospitality, teaching. Investment income covers most of your outgoings, the part-time work covers the rest, and you get your time back years before a traditional retirement date would allow.

Listen To This Podcast ????

Join us with Jon & David from The Debt Free Guys who went from 51k in debt to financially free in just 2 years!

How to Calculate Your Barista FIRE Number

Your Barista FIRE number is the pot of money you need invested to cover your living expenses, minus whatever you’re going to earn from part-time work.

The maths is genuinely simple.

The formula:

Barista FIRE number = (annual expenses ? part-time income) × 25

The × 25 bit comes from the 4% rule.

It assumes that if you withdraw 4% of your portfolio each year (and it’s invested in a diversified global equity and bond mix), historically your pot has lasted 30+ years in most starting market conditions.

It’s a rough rule, not a promise.

The original Trinity Study looked at US markets.

UK returns have historically been slightly lower, so some UK FIRE planners use a 3.5% rule to be safer, which means × 28 instead of × 25.

Two quick worked examples:

If your annual spend is £30,000 and you plan to earn £12,000 from part-time work, you need (£30,000 ? £12,000) × 25 = £450,000 invested.

If your annual spend is £40,000 and you plan to earn £8,000 from part-time work, you need (£40,000 ? £8,000) × 25 = £800,000 invested.

This is where the Barista FIRE calculator does the heavier lifting.

It accounts for inflation, investment growth, and the timeline from where you are now to where you need to be.

For a back-of-the-envelope calculation, the formula above will get you 90% of the way there.

Want your exact number?

Plug your salary, expenses, current savings and target part-time income into our Calculator.

It handles the inflation and growth assumptions for you and shows you the year you’ll hit the number.

Barista FIRE in the UK: ISAs, SIPPs and Tax

One thing most Barista FIRE content online gets wrong for UK readers: it’s written for Americans with 401(k)s, Roth IRAs and health insurance premiums.

In the UK you’ve got cleaner tools and a different timeline.

The tax wrappers that matter:

Stocks and Shares ISA: Your primary Barista FIRE vehicle pre-55. £20,000 annual allowance. Withdrawals are tax-free at any age. This is where the first decade of part-retirement income is going to come from.

SIPP: Tax-relief on contributions going in (25% uplift at basic rate, more if you’re higher rate).

Can’t access until age 55 (or 57 from 2028). Your “second phase” income once you’re 55/57+.

Lifetime ISA* If you’re under 40 and opened a LISA, it’ll pay out from age 60 with the 25% government bonus.

Useful, but not your main vehicle.

General Investment Account: Once you’ve filled your ISA and SIPP each year, the GIA is where extra savings go.

You pay CGT on gains and dividend tax on income. Less efficient, but uncapped.

The practical UK Barista FIRE sequence:

1. Max the ISA every year until you hit your number

2. Contribute to a SIPP for the tax relief, especially if you’re a higher-rate payer (it’s effectively 40% free money on the way in)

3. Once you pull the trigger on Barista FIRE, draw from the ISA first (tax-free, flexible, no penalty) and leave the SIPP compounding

4. At 57+, switch to drawing from the SIPP (25% tax-free lump sum, rest taxed as income)

5. Your part-time work income uses up some or all of your £12,570 personal allowance so you can potentially draw SIPP income tax-free if you keep your part-time earnings below it

NHS angle: Unlike US Barista FIRE, you don’t need to factor in health insurance.

The NHS is there. If you want private cover as a top-up (dental, faster diagnostics) that’s a budget line rather than a financial planning blocker.

National Insurance: If you stop full-time work before qualifying for a full state pension (35 years of NI contributions currently), your part-time work needs to earn above the lower earnings limit (£6,396 in 2026) in enough years to keep banking qualifying years.

Worth tracking on your gov.uk NI record.

Worked Examples: Three Realistic UK Barista FIRE Scenarios

These are three examples based on real-ish UK numbers. I’ve kept them mid-range and deliberately unsexy. No “ran a tech startup and sold it” fantasies. Just ordinary savings rates applied consistently.

| Age now | 32 |

| Annual expenses | £28,000 |

| Target part-time income | £10,000 (freelance design work, 2 days a week) |

| Barista FIRE number | (£28,000 ? £10,000) × 25 = £450,000 |

| Current savings | £45,000 |

| Monthly investment | £1,200 (ISA + SIPP) |

| Expected return | 8% per year (historical long-run average) |

| Time to Barista FIRE | ~13 years |

| Hit Barista FIRE at age | 45 |

| Age now | 36 |

| Annual expenses | £42,000 |

| Target part-time income | £12,000 (tutoring + small consulting) |

| Barista FIRE number | (£42,000 ? £12,000) × 25 = £750,000 |

| Current savings | £85,000 |

| Monthly investment | £1,800 (max ISA + partial SIPP) |

| Expected return | 8% per year (historical long-run average) |

| Time to Barista FIRE | ~14 years |

| Hit Barista FIRE at age | 50 |

| Age now | 28 |

| Annual expenses | £22,000 |

| Target part-time income | £8,000 (yoga teaching, 10 hours/week) |

| Barista FIRE number | (£22,000 ? £8,000) × 25 = £350,000 |

| Current savings | £18,000 |

| Monthly investment | £900 (max ISA only, low tax band) |

| Expected return | 8% per year (historical long-run average) |

| Time to Barista FIRE | ~15 years |

| Hit Barista FIRE at age | 43 |

The pattern is clear: your Barista FIRE age is driven more by your savings rate than by how much you earn.

Someone on £35k saving 30% of take-home will hit Barista FIRE at roughly the same age as someone on £70k saving 20%.

This isn’t a morally-loaded point. Just the compounding maths.

To run your own scenario with your own numbers, the Barista FIRE Calculator handles the inflation adjustment and shows you the exact year you’d hit the number.

Disclaimer: These examples use an 8% annual return, which reflects the historical long-run average for global equities over 100+ year rolling periods. Actual returns in any individual decade vary significantly, and past performance doesn’t guarantee future results. The figures are nominal (before inflation), so the real purchasing power of your Barista FIRE pot will be lower than the headline number. These worked examples are for illustration. None of this is financial advice. Capital is at risk when you invest.

How to get to Barista FIRE

- Clear expensive debt first. Anything above roughly 6-8% interest works against your investment returns and pushes your Barista FIRE number up.

- Push your savings rate, not just your income. The worked examples above show savings rate matters more than salary, so automate transfers on payday.

- Invest for growth, not cash. A diversified global equity and bond mix inside your ISA and SIPP is what makes the 4% rule (or 3.5%, for a safer margin) work over 25-30 years.

- Build side income options now, not after you quit, so you know the plan is realistic before you rely on it.

- Keep an emergency fund of at least three months’ expenses, so a bad month doesn’t force you to dip into the pot that’s meant to be compounding.

- Have a plan B. Markets fall and part-time work can dry up. Decide in advance what you’d cut or delay if either happens in your first year or two.

The pros and cons of Barista FIRE

Barista FIRE pros:

- You can leave full-time work years, sometimes decades, before a traditional retirement date, while keeping some income coming in

- The pot you need is smaller than full FIRE, often 40-60% less, because part-time income covers part of your expenses

- You stay engaged in work you actually choose, rather than facing a hard stop with nothing to fill the time

- You keep flexibility to dial part-time hours up or down as circumstances change

Barista FIRE cons

- You still rely on part-time income turning up, so you're not fully independent of employment

- There's less room for frugality than Lean FIRE but less spending power than Fat FIRE, so budgeting discipline still matters

- Part-time or freelance work can be inconsistent, which makes income planning harder than a fixed salary

- Stepping back early can mean a longer gap before you qualify for a full state pension, worth checking against your NI record

Barista FIRE vs Lean FIRE vs Coast FIRE vs Fat FIRE

The one people mix up most is Coast FIRE. The difference is when you stop saving: Coast FIRE means you’ve invested enough that compounding alone gets you to a traditional retirement date, so you stop contributing but keep working full-time until then. Barista FIRE means you step back from full-time work now and cover the gap with part-time income.

Quick reference:

- Lean FIRE: full retirement on a minimal, frugal budget

- Coast FIRE: stop saving, keep working full-time, let compounding finish the job

- Barista FIRE: part-retire now, cover the gap with part-time work (this guide)

- Fat FIRE: full retirement with no cut to lifestyle, the largest pot of the four

Full breakdown of how all four fit together in our FIRE movement guide.

Barista FIRE: Your Questions Answered

Barista FIRE is the retirement strategy where you save enough that a 4% withdrawal from your portfolio covers most of your living expenses, and you cover the remaining gap with part-time work. It sits between Lean FIRE and Fat FIRE.

Use the formula (annual expenses ? part-time income) × 25. For a £30,000 spend and £10,000 part-time income, that’s £500,000. Higher earners with higher spend need more. Our calculator handles the inflation adjustment.

Yes. Arguably more realistic than in the US, because you don’t need to budget for private health insurance. The ISA and SIPP combination also makes the tax-efficient drawdown cleaner than the US equivalent.

Coast FIRE is when you stop saving but keep full-time work until traditional retirement. Barista FIRE is when you partially retire now and cover the gap with part-time income. Different problem, different solution.

The 4% rule says if you withdraw 4% of your portfolio each year (invested in a diversified global equity/bond mix), it historically lasts 30+ years. UK returns have historically been slightly lower than the US data the rule was based on, so some UK FIRE planners use 3.5% instead.

(Annual expenses minus part-time income) times 25. Our Barista FIRE Calculator does this with inflation and growth assumptions built in.

Both. ISA first for the pre-55 income (tax-free withdrawals, flexible). SIPP for the tax relief going in and the post-57 income. Our full UK tax wrapper breakdown is in the section above.

Tutoring, freelance design, consulting in your old industry, bar work, yoga teaching, driving, teaching assistant work. Anything flexible and low-stress. The “barista” is a metaphor, not a requirement.

Yes, but factor the mortgage into your annual expenses. Some Barista FIRE plans pay off the mortgage first (usually a good move in the current rate environment), others keep it and factor the payment into the expense side of the formula.

Yes. The state pension (currently £241.30/week from 2026 at full rate) kicks in at 66 or 67 depending on your birth year. If you’re planning Barista FIRE in your mid-40s to mid-50s, bridge your ISA and SIPP to cover you until state pension age, then the state pension reduces your required withdrawal rate from there.

Should You Go Barista FIRE? My Take

For most people I speak to in the UK, Barista FIRE is the version of FIRE that actually works.

Full FIRE asks you to build a £1m+ pot and stop earning completely, which is both a long slog and psychologically harder than people admit.

Barista FIRE asks you to build maybe 40-60% of that, and then cover the gap with work you actually want to do.

The bit that’s worth stress-testing before you commit: whether you genuinely want part-time work, or whether you just want full retirement and are telling yourself part-time work is fine because the number is smaller.

Those are two very different plans.

Run the calculator for both.

If the Full FIRE number is a decade further away, ask yourself whether that decade is worth more than the part-time work you’d have to do in the Barista FIRE scenario.

My own take: I like the structure of part-time work in principle. Full retirement without a project to aim at has not gone well for most of the people I know who tried it. Barista FIRE gives you the freedom without the void.

Next steps:

Run your Barista FIRE number on the calculator

Compare it against Coast FIRE

Read the Lean FIRE guide if you want the minimalist version

Share on social media

Disclaimer: Content on this page is for informational purposes and does not constitute financial advice. Always do your own research before making a financially related decision.