Sammie Ellard-King

I’m Sammie, a money expert and business owner passionate about helping you take control of your wallet. My mission with Up the Gains is to create a safe space to help improve your finances, cut your costs and make you feel good while doing it.

Quickfire Roundup:

Remortgaging for an extension allows homeowners to capitalise on increased property value by borrowing against their home’s equity to finance expansions.

This can add value and space to the property while potentially offering better mortgage rates and avoiding the costs of moving.

I have always dreamed of adding more space and value to my home, and recently, I discovered the concept of remortgage for an extension.

The process isn’t as difficult as it might sound but there are some important things you need to consider and watch out for.

Remortgaging for an extension allows homeowners to borrow additional funds against the equity in their property, which can then be used to finance the cost of building an extension.

In this article, I will delve into the details of remortgaging for an extension, including the benefits, considerations, and how to go about the process.

- Sammie’s Number 1 Tip:

Speak to as many contractors and lenders as possible to get a full understanding of your costs for both the build and the remortgage. Taking my time to review the options literally saved me thousands of pounds.

Boon Brokers are one of the UKs leading online mortgage brokers. They have a 5-star excellent Trustpilot rating with over 543 reviews.

- No mortgage fees

- Whole of market access

- Free online consultations

- Directly authorised by the FCA

- No in person meet ups

Table of Contents

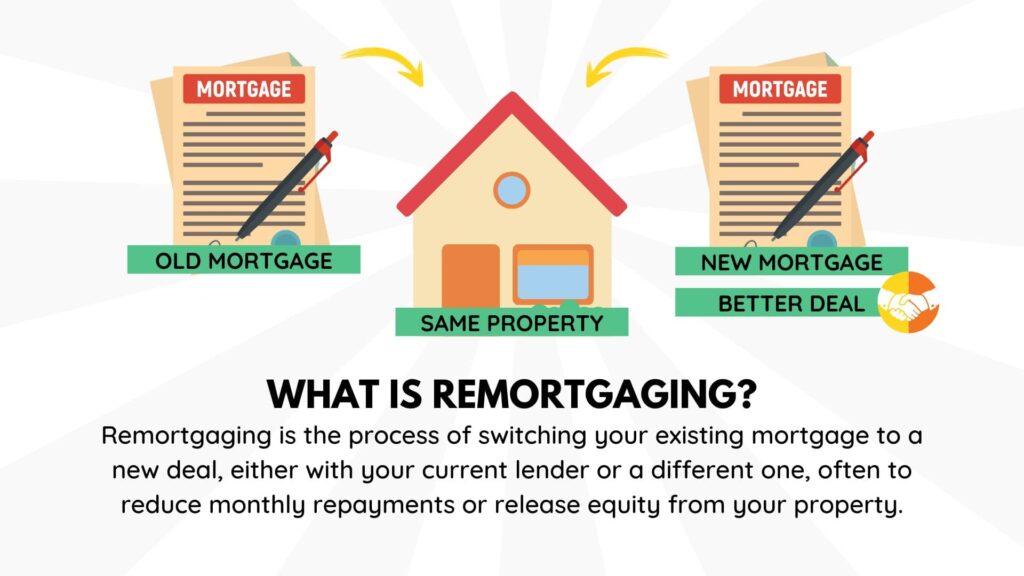

Understanding Remortgaging for an Extension

Remortgaging for an extension involves replacing your existing mortgage with a new one while borrowing additional funds to finance the extension.

By remortgaging, you can take advantage of any increase in the value of your property over time and release some of the equity to fund your home improvement project.

If your house has increased in value you are essentially extracting your profits to improve your current property which in turn will add more value.

This approach allows you to spread the cost of the extension over a longer mortgage term, potentially making it more affordable in the short term.

Reasons to Remortgage for an Extension

1. Add Value to Your Home

One of the main reasons homeowners consider remortgaging for an extension is to add value to their property.

By extending your home, you can create additional living space, such as an extra bedroom, study, or a larger kitchen.

These improvements not only enhance your quality of life but also increase the value of your home, making it more appealing to potential buyers in the future.

Essentially we’d all like to make money from our property and extensions are great ways to do that.

2. Create More Space

If you’re feeling squeezed for space in your current home, remortgaging for an extension can be a viable solution.

Whether you need a dedicated workspace, a playroom for the kids, a larger kitchen for entertaining or simply more room to relax, building an extension allows you to create the space you need without the hassle of moving to a new property.

3. Avoid Moving Costs

Moving to a new home can be a costly and stressful experience. In addition to the financial burden of buying a new property, there are also other expenses involved, such as stamp duty, legal fees, and removal costs.

Remortgaging for an extension provides an alternative solution that allows you to stay in your current home while still achieving your desired living space and adding value.

Things to Consider Before Remortgaging

While remortgaging for an extension can offer many advantages, it’s important to carefully consider a few key factors before committing to the process.

Here are some important points to keep in mind:

1. Affordability

Before remortgaging for an extension, it’s crucial to assess your financial situation and determine whether you can afford the additional borrowing.

Consider your current income, expenses, and any potential future changes that may impact your ability to make mortgage repayments.

It’s advisable to consult with a mortgage advisor who can analyse your financial situation and help you understand the affordability aspect.

2. Equity in Your Property

To remortgage for an extension, you will need to have sufficient equity in your property.

Equity is the difference between the current market value of your property and the outstanding balance on your mortgage.

Lenders typically have specific requirements regarding the minimum amount of equity you must have to qualify for a remortgage for an extension.

According to Finder, providers will look for at least 20% of your property in equity or a significant increase in property value. Anything less you may be required to get a guarantor or put up some other kind of asset.

Essentially it is a lot harder to remortgage without a good amount of equity.

3. Loan-to-Value Ratio

Another factor to consider is the loan-to-value (LTV) ratio. The LTV ratio represents the percentage of your property’s value that you’re looking to borrow. Generally, lenders prefer lower LTV ratios, as they consider them less risky.

Therefore, if you’re looking to borrow a significant amount for your extension, you may need to ensure that your LTV ratio is within acceptable limits.

4. Creditworthiness

Lenders assess your creditworthiness when considering your remortgage application. Lenders look for a good credit score and a history of responsible financial behaviour can increase your chances of securing a favourable remortgage deal.

On the other hand, if you have a history of missed payments or have significant debts, you may find it more challenging to secure the necessary funds.

5. The Build

Something I don’t think is factored in enough is the extension build. The average extension according to My Bespoke Room takes between 8-16 weeks depending on the size.

Equally to add space often the current structure of the home will need to be altered so key rooms in the house are essentially out of action for larger periods of time.

For instance, you may be extending the kitchen which means the entire current kitchen will be remodeled leaving you without key appliances.

That means ordering takeaways, using facilities at the gym or relying on friends and family for hygiene or cooking, often months at a time.

Just to be clear self-build mortgages are not something that you can consider here as they are for new property builds.

The Process of Remortgaging for an Extension

Once you’ve carefully considered the factors mentioned above and decided to proceed with remortgaging for an extension, it’s time to understand the steps involved in the process.

Here is a general outline of what you can expect:

1. Evaluate Your Options

Start by researching and comparing different mortgage lenders and their remortgage products.

My tip which I found very useful was to speak to lenders who specialise in home improvement and extension loans, as they may offer more favourable terms.

Then make sure you consider factors such as interest rates, fees, repayment terms, and customer reviews to find a lender that suits your needs.

2. Consult with a Mortgage Advisor

To navigate the complexities of remortgaging for an extension smoothly, it’s advisable to seek guidance from a qualified mortgage advisor.

They can help you understand the various options available, evaluate your financial situation, and guide you through the application process.

I spoke to 4 lenders directly myself but the mortgage advisors have access to the entire market and can often see via a portal who has the best mortgage rates available.

Be sure to ask your mortgage advisor questions and feel comfortable you are choosing the right lender based on your needs.

3. Determine the Cost of the Extension

Before finalising your remortgage plans, it’s essential to have a clear understanding of the cost involved in building your desired extension.

Obtain quotes from reputable builders or architects to ensure that you have an accurate estimate of the expenses.

- My hot tip:

Get more than 1 quote – I got at least 5 from multiple builders and then negotiated based on the averages. Some builders literally come in £5k higher than others so it’s worth it for you wallets

4. Apply for the Remortgage

Once you have selected a lender and have a good idea of the extension cost, it’s time to apply for the remortgage.

Prepare all the necessary documentation, such as proof of income, bank statements, and identification.

Your mortgage advisor can assist you with the application process, ensuring that all the required information is submitted correctly.

Our mortgage advisor held our hand throughout the entire process and filled in most of the paperwork on our behalf after we had a Zoom meeting with them.

5. Valuation and Legal Processes

After receiving your remortgage application, the lender will arrange a valuation of your property to determine its current market value.

They will also conduct the necessary legal processes to complete the remortgage. Depending on the complexity, this stage may take a few weeks to complete.

6. Releasing the Funds and Building the Extension

Once the remortgage is approved, the lender will release the additional funds. You can then engage builders and contractors to start the extension project.

It’s important to have a realistic timeline in place and ensure regular communication with the contractors to ensure the project stays on track.

Be sure to lock in the price with the builder so you’re not subject to fluctuations in building costs or hidden costs that are unforseen during the build.

7. Repayment and Future Considerations

After your extension is completed, you will need to start making repayments according to the terms and conditions of your new mortgage.

I think it’s vital to review your financial situation periodically and consider any future changes that may impact your ability to meet the mortgage obligations.

Pros & Cons of remortgaging

Pros of remortgaging for an extension

- Increased Property Value: Extending your home can significantly increase its value. If done correctly, the value added can be more than the cost of the extension.

- Cost-Efficient: It can sometimes be more cost-effective to extend your existing property than to move to a bigger one, especially when considering costs such as stamp duty, agency fees, and removal expenses.

- Better Rates: If your initial mortgage deal has ended and you’re on your lender’s standard variable rate (SVR), remortgaging might get you a better interest rate. This can result in lower monthly repayments.

- Consolidation: Remortgaging can allow you to consolidate other debts, leading to potential interest savings and easier financial management.

- Customisation: Extending allows you to design the space to your specific needs and desires.

- Avoiding the Hassle of Moving: By extending instead of moving, you can avoid the stress, costs, and disruption that come with relocating.

Cons of Remortgaging for an Extension:

- Overcapitalisation: There’s a risk that the cost of the extension may not be fully reflected in the increased value of your home, especially if the improvements are too unique or if the market conditions deteriorate.

- Higher Total Interest: By increasing the size of your mortgage, you could end up paying more interest over the long term.

- Extended Loan Term: Remortgaging might mean extending the term of your loan, which means it’ll take longer to become mortgage-free.

- Costs and Fees: Remortgaging comes with its own set of costs – valuation fees, arrangement fees, legal costs, and potential early repayment charges on your existing mortgage.

- Potential for Negative Equity: If property prices fall, you risk being in negative equity, especially if the remortgage value is close to the current value of your home.

- Affordability Checks: Just because you were approved for your initial mortgage doesn’t guarantee that you’ll be approved for a remortgage, especially if your circumstances have changed.

- Disruption: Building an extension can be disruptive, noisy, and stressful. It can take longer than anticipated and there might be unforeseen complications or expenses.

FAQs

Can I remortgage for an extension with bad credit?

Yes, it is possible to remortgage for an extension if you have bad credit.

However, having bad credit may limit your options and make it more challenging to find a lender who will offer favourable terms.

It’s advisable to consult with a mortgage advisor who specialises in bad credit remortgages to explore your options.

Do I need planning permission for my extension?

No, not necessarily but there are occasions when you will need permissions.

Whether or not you need planning permission for your extension depends on various factors, such as the size and location of the extension.

In some cases, certain types of extensions may fall under permitted development rights and not require formal planning permission. However, it’s always recommended to check with your local planning authority to ensure compliance with regulations.

How much equity do I need to remortgage for an extension?

The amount of equity required to remortgage for an extension can vary depending on the lender and their specific criteria.

Generally, lenders prefer borrowers to have a minimum of 20% equity in their property. However, each lender may have different requirements, so it’s best to consult with a mortgage advisor to determine the exact amount of equity you need.

Can I remortgage to fund other home improvements?

Yes, remortgaging can be a viable option to fund other home improvements besides extensions.

Whether you want to add value to your property with a kitchen renovation, loft conversion, or other upgrades, remortgaging allows you to release equity to cover the costs.

It’s important to consider the financial implications and ensure that the improvements are likely to increase the value of your property.

How long does the remortgaging process take?

The remortgaging process can vary in duration, depending on several factors, such as the complexity of your financial situation and the lender’s efficiency.

On average, the remortgage process can take between four to eight weeks. It’s advisable to start the process well in advance of when you plan to start the extension project to allow sufficient time for all the necessary steps.

Conclusion

Remortgaging for an extension can be an excellent way to add value, create more space, and avoid the costs and stress of moving to a new property.

However, it’s important to carefully consider your financial situation, equity, and creditworthiness before committing to the process.

By understanding the steps involved and consulting with a mortgage advisor, you can navigate the remortgaging process smoothly and turn your extension dreams into a reality.

Share on social media

Disclaimer: Content on this page is for informational purposes and does not constitute financial advice. Always do your own research before making a financially related decision.