One of the first investing strategies a beginner learns is dollar-cost averaging, and with good reason, it’s effective.

It takes much of the guesswork out of your investing decisions, and history shows it works time and time again.

Table of Contents

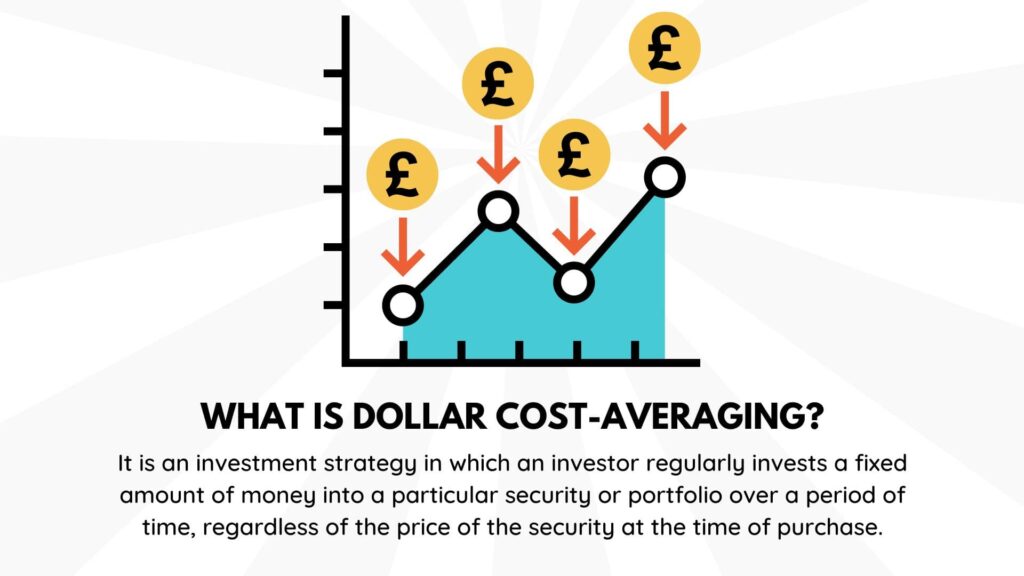

What is Dollar Cost Averaging?

Dollar-cost averaging is simply an investing strategy where an investor allocates a set amount of money at regular intervals to be invested. For example, if you have a retirement account and automatically deposit money into it each month, that is dollar cost averaging.

This strategy works partly because it automates the process of investing, and an investor does not need to follow market trends or business news for it to work. It’s simple and easy to follow.

How Dollar Cost Averaging Works?

Let’s have a look at a dollar cost averaging example.

Say you want to start investing in the stock market to save for your retirement. There are so many stocks to choose from, and studying them all, or even a fraction of them, would quickly become overwhelming.

In addition, every day, the stock market fluctuates. One day it’s up, the next day, it’s way down. Trying to time the market is impossible, and those who try just end up frustrated and burning themselves out.

Instead of trying to time things, an intelligent investor may commit to setting aside 10% of their monthly income and on the last day of the month, deposit that money into a brokerage account and buy shares of a mutual fund.

Whether the market is up or down, or there seems to be good news or bad news coming out of the financial press, the decision is always the same, 10% of income goes into a mutual fund.

We know the stock market goes up, then comes down, but overall steadily climbs in that signature zig-zag pattern.

When dollar-cost averaging, there will be times when investments are purchased right at a local top, only to see it drop in value the next day, and times when the bottoms are hit perfectly, and the investment appreciates in value the next day.

Over time, all the fluctuations will even out, leaving the investor with a nice steady gain. No guessing, no praying, and no market timing is needed, just an automated process and continuous, sustained growth.

Why Does a Dollar Cost Averaging Strategy Work?

The advantages of dollar cost averaging is that it is easy to follow, and there is no second guessing. It can be fully automated, so an investor can set it up and look at it once a year or so just to ensure things are progressing as they should.

History has shown that novice investors employing this strategy can reach their financial goals just as well as by using professionally managed funds.

How Does it Compare to Other Strategies?

Other strategies are available, and they are not all without merit. Dollar-cost averaging is not the only strategy available, although it is the easiest and will typically offer the highest chance of success for the work involved.

To get a better understanding of dollar-cost averaging, we should take a look at other strategies and compare how it stacks up.

How does it differ to a Lump Sum Deposit?

You may wonder how dollar-cost averaging would compare against a single lump sum purchase of a stock market investment. Dollar-cost averaging works because it removes the risk of making a significant investment right at the top of the market.

Doing so also takes away the chance of buying right at the bottom when it would be most profitable.

With a lump sum, you are taking on a risk that does not need to be taken. Sure, you may get lucky and buy at just the right time, but you may be unlucky and buy at the wrong time.

Dollar-cost averaging takes all that away, but as we know, slow and steady investments over a long period will leave an investor with enough money to reach their goals anyway.

Furthermore, an investor is unlikely to have a lump sum when starting anyway. Dollar-cost averaging works best when the money comes from your current income.

What is Value Averaging?

Value averaging is another strategy similar to dollar-cost averaging but has one more step. Value averaging attempts to take advantage of the market swings and earn a little better return than dollar-cost averaging.

When an investor employs this strategy, instead of a set amount per time interval, they commit to increasing the overall value of their investment per time interval.

Let’s say an investor is dollar-cost averaging and has £100 per week to invest. They simply buy £100 of the fund each week. A value-averaging investor may decide to increase their investment amount by £100 instead.

When using this strategy, they deposit £100 the first week, just like the dollar-cost averaging strategy. Then the market dropped 5% the following week.

The one using dollar-cost averaging would deposit £100, but the value averaging investor would deposit £105 to bring the total account value up to @200. Had the market gone up 5%, they would deposit £95.

It is easy to see what value averaging is trying to accomplish that dollar-cost averaging does not. It is attempting to take advantage of the market swings by buying a little more when the market dips and a little less when it rises.

In theory this can provide you with a lower average and in turn better results.

How Value Averaging works?

At first, this may seem like a brilliant idea, but those practising it will soon become a big problem. It takes advantage of the market’s irregular action and may result in better returns over the first few months.

The problem lies in deciding how much the balance should increase each week, month, or whatever the time interval is. With dollar-cost averaging, it’s easy. If an investor has £150 a month, they should deposit £150.

But let’s say the same investor wants to employ the value averaging strategy. What number should they choose, and how should they choose it?

If they decide on £150, as soon as there is a market decline, they will not have enough cash to make the next purchase. At that point, all they will be able to do is add the £150 they have, which essentially means they are back to dollar-cost averaging.

For value averaging to really work, an investor must know what the future market action will be to correctly decide how much they should make their investments increase each month, which is, of course, impossible.

Choose a number too big; eventually, they run out of cash and are left dollar-cost averaging, and choose a number too small, and they are left with uninvested funds that should be growing.

Value averaging sounds good, but it is impossible to execute correctly in practice all of the time.

DCA, Technical and Fundamental Analysis

You may now wonder if you are leaving money on the table by not learning about and employing the fundamental and technical analysis strategies many investors like to learn about.

Clearly, people are making enormous sums of money by doing more than dollar-cost averaging. Hedge funds in New York, London, Singapore and all of the world’s financial hubs employ thousands of analysts, all trying to outperform the market and their peers with complex trading strategies.

Certainly, some of them are successful and go on to achieve wild riches. But many fail and lose everything as well.

Dollar-cost averaging works because it eliminates the possibility of losing money over a long enough period. Sure there may be a cap to the upside, but the cap is well above what most people will need in order to hit their most important goals.

Conclusion

You may be wondering if dollar cost averaging is the only strategy you should be using. Well, it may be, and if you are only going to use one strategy, it should, without a doubt, be dollar-cost averaging. But there is likely room in your overall portfolio to use other strategies.

What works well for many successful people is to make a list of all the truly important goals you have for your life and then estimate how much money you will need in order to achieve all of those goals.

For example, if you want a nice retirement, maybe send your kids to college and perhaps do some travelling. For that important pot of money, use the dollar-cost averaging strategy, and you are guaranteed not to make any crucial mistakes that cannot be recovered from.

If you have any other money left over, that money can be invested using different strategies. It’s always good to learn about things, and if you are curious or interested in learning about the stock market, have at it and buy some stocks you think may make you wealthy.

You may win; you may lose. But as long as you are using old, reliable dollar-cost averaging for the important money, you really have nothing to worry about.

Share this article with friends

Disclaimer: Content on this page is for informational purposes and does not constitute financial advice. Always do your own research before making a financially related decision.