The 11 Best Income-Generating Assets in the UK (2026)

1. Dividend Stocks

In case it’s not evident from the name, dividend-paying stocks are stocks that pay dividends to investors or shareholders in specific intervals. These payments are either cash or more shares of the stock.

Regular stocks only pay out when sold, but some large blue-chip companies (like Imperial Brands or Lloyds Banking Group) regularly pay profits to shareholders as dividends.

Learning how to invest in dividend stocks is very simple. You just need to check whether the company pays one and purchase the stock as normal. The stock will pay out at certain times on the year based on the amount you’ve invested.

Let’s take a look at an example.

A company is offering a 5% dividend yield. Its stock holds at £20/share for the year. If you own 100 shares in the stock, you’ll either receive £1/share in cash or buy five more shares through reinvestment over the year.

Just note that you can’t just pick stocks based on the dividend payments. You also need to consider:

Some sectors are known to have higher dividend yields, like utilities and consumer goods. These sectors are good places to start your investment journey.

On tax, you get a £500 tax-free dividend allowance each year, and any dividends earned inside a Stocks and Shares ISA are completely tax-free, so most investors hold their dividend shares in an ISA. Commission-free platforms like Trading 212 make it easy to start.

Capital at risk. Investments can fall as well as rise and you may get back less than you put in. This is not financial advice, always do your own research.

2. Digital Products

Digital products are anything that you make once but can be purchased an infinite amount of times online.

Products include items like ebooks, worksheets, mini courses, planners, Notion templates and so many more.

Learn how to create and sell digital products with our full guide.

They are housed on an online store for example like Shopify or StanStore and sold through Stripe or Paypal.

You can be up and running within a matter of days and use social media to promote your products. I’ve personally been selling an enormous amount of digital products this year with over £20,000 in sales.

The bulk of the money comes from social media but a good 30% of it comes from a mailing list.

It’s key to build this up but we have a course coming on it where you can learn how to go from idea to product launch in just a week and be making money in 21 days!

3. Physical real estate properties

I should begin by saying that real estate investing is very different from simply buying a house. This investment is an income-generating asset that can take several shapes:

Rental property: A rental property is a real estate asset that you buy with the sole purpose of renting it to tenants. You don’t plan on living in it yourself.

This kind of income-generating asset results in residual income each time your tenants pay rent. Long-term rentals ensure you have a steady income stream, but short-term rentals (like renting your property through Airbnb) can bring in more cash.

Commercial property: Shopfronts, offices, co-working spaces… these are all great options for investors to purchase. You can either purchase a property through a realtor or use a real estate crowdfunding platform to help you with your investment.

And, if you don’t feel like managing your rental properties yourself, you can always hire a property manager for a true hands-off investment.

However, there are some risks.

The success of rental properties often hinges on location and market trends. Properties in high-demand areas can yield significant rental income and appreciate in value, while those in less desirable areas may not perform as well.

Then there’s the volatility of the market. Any changes in demand for rental properties, economic downturns or local developments can impact rental prospects. Selling a property is also not always straightforward if you wish to quickly access additional funds.

You also need to be aware of taxes. If you own rental properties, the first £1,000 you earn from rental income is tax-free, thereafter you have to pay income tax.

Something else you can consider to get your foot in the real estate door is to rent out a room in your house (if you own it) to generate income without massive upfront investments.

Capital at risk. Investments can fall as well as rise and you may get back less than you put in. This is not financial advice, always do your own research.

4. Peer-to-peer lending

If you have some money to spare, then peer-to-peer (P2P) lending can be a great way to boost your income and make money.

P2P lending is aimed at borrowers who, for whatever reason, don’t want to take out a bank loan.

You can lend money to these individuals and earn income through interest on the loan repayments. Depending on the loans, you can earn annual returns between 4% and 10%.

Of course, there are some risks associated with P2P lending – the biggest one being that the borrower never repays their loan.

Most P2P lending platforms are regulated by the Financial Conduct Authority, which offers some protection to the lender but always be sure to check this and don’t deal with unregulated providers.

The best way to negate this risk of not receiving your money is to spread your investment across several loans.

You can hold many peer-to-peer loans inside an Innovative Finance ISA (IFISA) to earn the interest tax-free.

Capital at risk. Investments can fall as well as rise and you may get back less than you put in. This is not financial advice, always do your own research.

5. Local small business investing

Have you always had lofty dreams of being a business owner, but never had the inspiration to get started? One shape that income-generating assets can take is to invest in someone else’s small business.

You can approach business owners directly or use crowdfunding websites and filter by businesses close to you.

By investing in local businesses, you are contributing to the local economy. However, it’s important to carefully assess the potential risks.

There is one realistic downside to investing in small businesses: failure. Start-ups can be risky as they’re not yet established; however, if the business succeeds, the payouts can be incredible.

There are different types of small business investments you can make:

Equity investments: You buy a share in the company and earn a portion of the profits.

Debt investments: You can lend money to the start-up and the loan is repaid with interest.

Convertible investments: A combination of the two types above. Your loan can be converted into business shares.

Before you take on this kind of income-generating asset, you’ll have to do your due diligence. Analyse the company’s financial statements, make sure you understand the business model, consider the expertise of the management team, and make your decisions from there.

Capital at risk. Investments can fall as well as rise and you may get back less than you put in. This is not financial advice, always do your own research.

6. Savings accounts and Cash ISAs

If you want the simplest income-generating asset of the lot, a savings account is hard to beat. You hand your cash to a bank or building society, and they pay you interest on it. No markets, no volatility, and your money is protected up to £120,000 per institution by the FSCS (the limit rose from £85,000 in December 2025).

There are a few flavours worth knowing:

- Easy-access savings: withdraw whenever you like, usually the lowest rate. In June 2026 the best buys sit around 4.5% AER.

- Fixed-rate bonds: lock your money away for one to five years for a slightly higher, guaranteed rate. The top one-year fixes are around 4.85%.

- Cash ISA: the same idea, but the interest is completely tax-free. The best Cash ISAs pay around 4.75%. With rates higher than they were a decade ago, more people are breaching their Personal Savings Allowance, so a Cash ISA is doing real work again.

The trade-off is simple: your money is safe and the income is predictable, but the returns rarely beat inflation by much. Savings are best for your emergency fund and short-term goals rather than long-term wealth building. If you are weighing tax-free options, read cash ISA vs stocks and shares ISA.

Rates correct as of June 2026 and change regularly, always check the latest rate before you open an account.

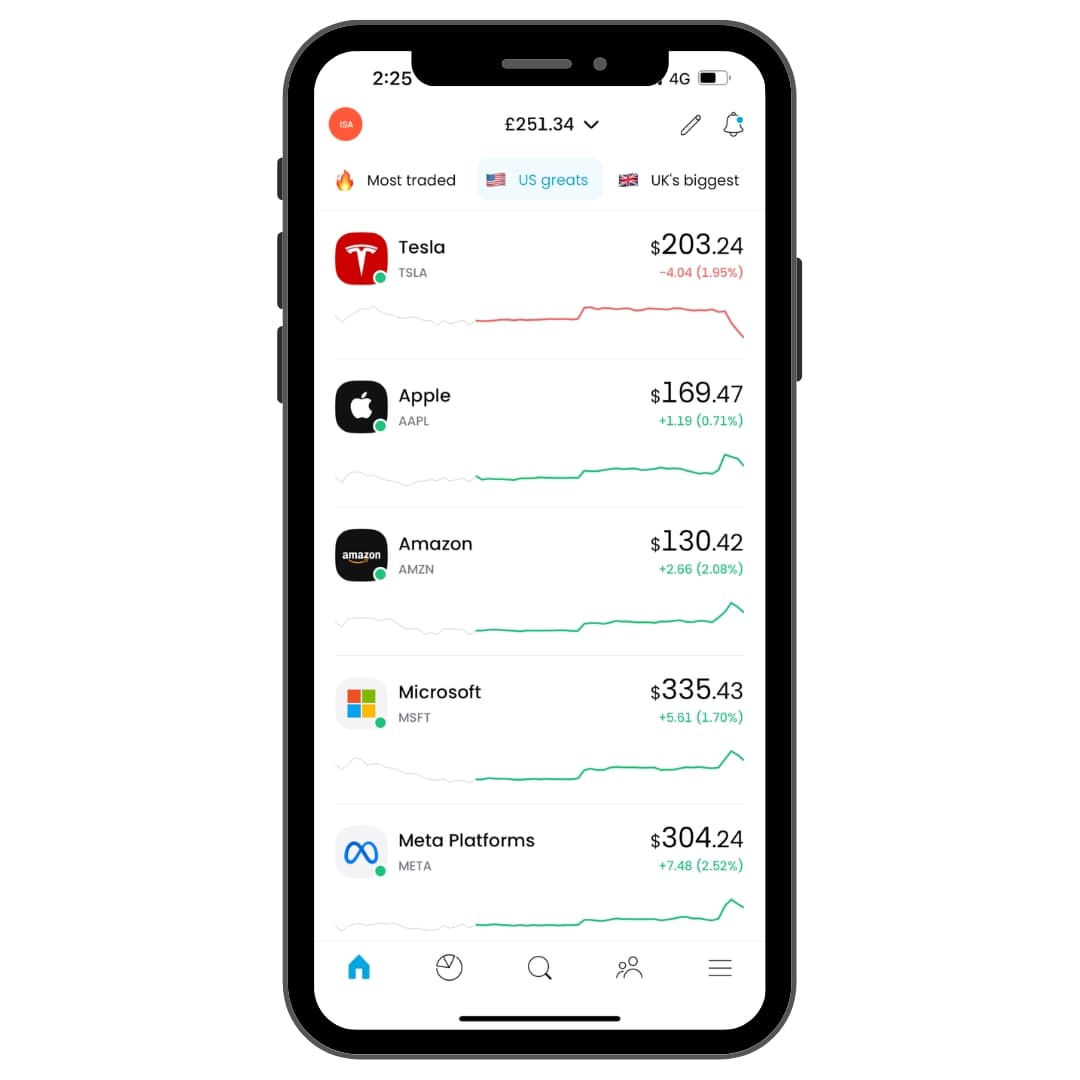

7. Index funds and ETFs

If you only ever learn about one asset on this list, make it this one. An index fund (or its close cousin, the exchange-traded fund) buys a tiny slice of hundreds or thousands of companies at once, tracking a whole market like the FTSE 100 or the S&P 500. You get instant diversification for a few pounds.

Here is how the income works. Funds come in two versions: income units pay the dividends out to you as cash, while accumulation units reinvest them automatically to compound your pot. A global index fund has historically returned somewhere around 7% a year on average over the long run, made up of share-price growth plus dividends. Past performance is not a promise, and values fall as well as rise, but for hands-off, long-term investing this is the engine most UK investors rely on.

The fees are tiny (often under 0.25% a year), you can start with as little as £1 on most platforms, and held inside a Stocks and Shares ISA or a SIPP your growth and income are tax-free. Commission-free platforms like Trading 212 let you buy index funds and ETFs without dealing fees. If you are new to it, start with our full guide on how to invest in index funds UK.

Capital at risk. Investments can fall as well as rise and you may get back less than you put in. This is not financial advice, always do your own research.

8. Private equity investing

Don’t run away when you hear the words “private equity” – it’s not just for the incredibly wealthy!

Private equity investing is when you invest in private companies. A lot of these companies are just starting to become established. It is very similar to the small business investing I discussed above. However, the main difference is that when you invest in small businesses, it’s often a local company and you directly interact with the owner.

When it comes to private equity, you invest in companies through a private equity firm. The firm will pool money from a variety of investors, and that money is then used to buy, manage and sell companies.

By working through a firm, you are able to spread your risk. You also don’t have to do your own research on which companies to invest in (which can be very difficult if you have no idea where to start).

In the UK, investing through EIS or SEIS-qualifying companies can also give generous income tax and capital gains tax relief, though these are high-risk, illiquid investments.

Capital at risk. Investments can fall as well as rise and you may get back less than you put in. This is not financial advice, always do your own research.

9. Government and corporate bonds

When you buy a bond, you are lending money to a government or a company in exchange for regular interest payments (called the coupon) and your original sum back at the end of the term. UK government bonds are known as gilts, and they are about as low-risk as investing gets, because the chances of the UK government failing to pay you back are very small.

Bonds had a quiet decade when interest rates were near zero, but that has changed. In June 2026 the 10-year gilt was yielding around 4.9%, which makes them a genuine income option again. Corporate bonds pay a bit more than gilts to compensate for the extra risk that the company runs into trouble.

You can buy individual gilts directly, or get exposure through a bond fund or ETF that spreads your money across hundreds of them. Bonds are the classic ballast in a portfolio: they tend to be steadier than shares and pay a dependable income, which is why investors often hold more of them as they get closer to needing the money. Held inside a Stocks and Shares ISA or SIPP, the income is tax-free.

Capital at risk. Investments can fall as well as rise and you may get back less than you put in. This is not financial advice, always do your own research.

10. Real estate investment trusts

Before telling you why you should consider a real estate investment trust (REIT), let me first briefly explain what it is.

A REIT is a company that buys, sells, maintains and manages commercial real estate properties. By investing in a REIT, an investor (i.e. you) earns passive income from rent collected.

REITs can cover a variety of property types, including:

Having this variety of properties results in a diversified portfolio. Actually, investing in REITs is a good way to diversify your portfolio if you’re also investing in dividend stocks, mutual funds and bonds.

REITs are perfect for those who don’t want to buy and manage their own properties. This way, you’ll also forego the massive downpayment on a property.

Usually, REITs pay high dividends. Some are traded on the stock market, while others are not. If you’re new to investing, you’re going to want to stick to publicly traded REITs because of better governance standards and transparency. You can purchase these through online brokers.

The biggest risk when investing in a REIT is market fluctuations. Economic downturns can cause property values – and rental income – to drop.

REITs themselves are exempt from corporation tax on their profits earned from rental income.

In the UK, big names include British Land, Segro and Land Securities, and because REITs trade like shares you can hold them inside a Stocks and Shares ISA to take the income tax-free.

Capital at risk. Investments can fall as well as rise and you may get back less than you put in. This is not financial advice, always do your own research.

11. Premium Bonds

Premium Bonds are a uniquely British way to earn on your savings. Run by NS&I and backed by the Treasury, they do not pay interest in the normal sense. Instead, every £1 bond is entered into a monthly prize draw, and you can win anything from £25 to £1 million, completely tax-free.

The prize-fund rate rises to 3.80% from the July 2026 draw (up from 3.30%), with odds of 22,000 to 1 for each £1 bond. That rate is an average across all bondholders, not a guarantee. Plenty of people win nothing for months, while a lucky few win big. You can hold between £25 and £50,000, your capital is 100% safe, and you can cash out at any time.

Premium Bonds are best thought of as a fun, tax-free home for cash you want kept safe rather than a serious income engine, especially if you have already used your Personal Savings Allowance. For a full breakdown of the odds, see are Premium Bonds worth it.

Rates correct as of June 2026 and change regularly, always check the latest rate before you open an account.

FAQs

What are income-generating assets?

An income-generating asset is something you own that pays you a regular return, on top of any rise in its value. Dividend stocks pay dividends, property pays rent, bonds and savings pay interest, and index funds pay both growth and dividends. The goal is to build a mix so money flows in without you trading your time for it.

What are the best income-generating assets in the UK?

For most UK investors the core options are dividend stocks, index funds and ETFs, buy-to-let property, REITs, government and corporate bonds, peer-to-peer lending, and cash in savings or a Cash ISA. The right blend depends on your goals, timeframe and risk appetite. Wrapping them in a Stocks and Shares ISA or SIPP keeps the income tax-free.

What are good income-generating assets for beginners?

Start simple and low-risk. A Cash ISA or easy-access savings account, then a global index fund inside a Stocks and Shares ISA, covers the basics with very little to manage. Add dividend stocks, REITs or bonds as your confidence grows. You do not need a fortune, most platforms let you start from £1.

Why should I invest in income-generating assets?

Investing in an income-generating asset offers you the following benefits:

- Regular cash flow

- Financial freedom

- Increase your net worth

- Change your lifestyle

- Start building generational wealth

Where do I start if I want to buy an income-generating asset?

The best step for complete beginners is to start with low-risk options so you can learn as you go. In the UK that usually means easy-access savings accounts, a Cash ISA or fixed-rate bonds. Once you are more comfortable, you can move on to index funds, REITs, dividend stocks and eventually rental property.

How much money do I need to start investing?

You don’t need to have a fortune to start investing. A lot of income-generating assets can be started with modest amounts of money.

The key is to begin investing with what you’re comfortable with and make sure you still have enough money to survive. You can always increase your investment as you improve your investment knowledge.

How can I balance risk and reward when investing in income-generating assets?

Knowing how to balance risk and reward is key when you start out. Begin with low-risk options like savings accounts, Cash ISAs or gilts, and always research the risks before investing. As you grow more confident, you can diversify into higher-risk, higher-return assets like index funds, shares and property.

Final Thoughts

Here’s my secret: The smartest financial decision you’ll ever make is to invest in any of the best income-generating assets listed above.

An income-producing asset can earn you passive income, as long as you put your money in the right place. You may have to make some initial investments – like putting a minimum amount in a savings account or purchasing a property – but income-producing assets will ensure you receive a steady stream of money.

I truly believe that investing will be one of the best decisions of your life when it comes to your personal finances.

For beginners, it is key to build a diverse investment portfolio. REITs, rental income and blue-chip stocks can all be low-risk options with high annual returns. Now, all you need to do is get started.

Share on social media

Disclaimer: Content on this page is for informational purposes and does not constitute financial advice. Always do your own research before making a financially related decision.