Sammie Ellard-King

I’m Sammie, a money expert and business owner passionate about helping you take control of your wallet. My mission with Up the Gains is to create a safe space to help improve your finances, cut your costs and make you feel good while doing it.

Quickfire Roundup:

The average monthly savings for a single person in the UK is around £180-200, and the current average household savings are £450 per month.

This suggests that saving £200 a month is right on par with the average if you’re doing it alone and falls slightly under the average for a UK household.

At this level, while it may not be above average, it’s a consistent and achievable amount for many, which means it can still make a notable difference in your financial future if you keep at it.

So, where does £200 a month actually get you? Let’s explore.

Is Saving £200 A Month Good Enough? Well, the answer depends on individual circumstances.

For the everyday person, £200 a month is a reasonable amount to set aside.

While you might want to put more away, it’s an excellent starting point and far better than saving nothing at all in my opinion.

Always consider how this amount aligns with your living expenses, your current financial circumstances, and your long-term goals.

Every bit adds up, so let’s make that £200 meaningful on your journey toward financial stability.

Table of Contents

Is Saving £200 a Month Good in the UK?

Setting aside £200 each month adds up to £2,400 annually, which is no small feat and can substantially bolster your financial reserves.

If you’re consistent with your monthly contributions, you’ll gradually amass a meaningful nest egg.

Considering various interest rates is worthwhile; you could also consult with a financial advisor or money coach if you’re not sure how best to maximise your savings.

Once you’ve accumulated a robust emergency fund, the next sensible move would be to start investing a considerable portion of this money. Solidifying your grasp of personal finance can truly make a difference here.

Let the latest technology help get you there with the best money savings apps.

🎙️ Listen To This Podcast Episode 🎙️

Join me with Catherine Cornwall, Money Coach and Hypnotherapist!

We discuss how your roots have an impact on your savings and investments, the power of self awareness for your spending habits, how to deal with bad money habits and SO MUCH MORE!

Get the full episode by clicking here name just above or go to The Money Gains Podcast page here.

How Quickly Does £200 Grow with Different Interest Rates?

Let’s examine various interest rate scenarios to see the long-term effects on your returns.

| Years | 1% Annual Rate | 2% Annual Rate | 3% Annual Rate | 4% Annual Rate | 5% Annual Rate |

|---|---|---|---|---|---|

| 1 | £2,424 | £2,448 | £2,473 | £2,498 | £2,523 |

| 2 | £4,897 | £4,995 | £5,092 | £5,192 | £5,292 |

| 5 | £12,412 | £12,658 | £12,908 | £13,164 | £13,424 |

| 10 | £25,620 | £26,497 | £27,403 | £28,341 | £29,312 |

| 20 | £54,805 | £58,814 | £63,119 | £67,734 | £72,701 |

| 30 | £90,721 | £100,355 | £110,726 | £122,030 | £134,336 |

As illustrated by this table, a slight uptick of just 1% in interest rates can have a profound impact on your eventual returns.

Why is that? It’s all down to the magic of compound interest: your interest accrues interest, and over time, this compound effect really starts to gather momentum.

Let the latest technology help get you there with the best money savings apps.

Why £200 a Month?

So, is saving £200 a month good in the UK? The figure of £200 a month frequently appears in personal finance chatter, and for good reason.

It serves as a manageable yet impactful sum for many.

Whether you’re eyeing short-term financial resilience or long-term fiscal freedom, £200 a month can genuinely make a difference.

Let’s dig into the key areas where this monthly sum proves to be particularly effective.

Financial Resilience

Consistently putting away £200 a month creates a financial cushion that can come in handy when life throws curveballs at you.

Accumulating £2,400 within a year provides you with a safety net for unforeseen expenses, be it an urgent car repair or sudden healthcare costs.

For many, having this financial buffer provides the peace of mind that they won’t be easily upended by unexpected financial challenges.

Achievable Financial Goals

With a commitment of £200 a month, reaching your financial goals starts to look much more feasible.

Whether you’re saving for a holiday, your wedding, or even launching your own venture, knowing you have a set amount to save each month provides a structured approach to your financial planning.

A consistent strategy makes even ambitious financial objectives seem within reach.

Journey Towards Financial Independence

If you have your eyes on the Financial Independence, Retire Early (FIRE) movement, our handy FIRE calculators can show the potential impact of a £200 monthly savings habit.

This level of regular saving can significantly speed up your path to financial independence, granting you greater freedom to live life as you wish.

Stepping Onto the Property Ladder

In the UK context, stepping onto the property ladder is often considered a major financial accomplishment.

While the average UK deposit may seem daunting at around £53,935, saving £200 a month consistently can make this target more attainable.

In just over 22 years, you’d reach that average deposit amount, not to mention the additional benefit of any interest or investment gains made during that period.

Preparing for Retirement

Last but by no means least, saving £200 a month can be a game-changer for your retirement nest egg.

Thanks to the magic of compound interest, your monthly contributions will accumulate into a significant sum over the years.

When retirement eventually comes calling, you’ll be grateful you stuck to that £200 monthly commitment.

Let the latest technology help get you there with the best money savings apps.

How Much Should I Save Each Month?

Striking the right balance for your monthly savings is often easier said than done.

Save too little, and you risk not meeting your financial goals; save too much, and daily living expenses could become a struggle.

This question doesn’t have a one-size-fits-all answer, but a few key considerations can help you tailor a saving strategy that suits your personal situation.

These include budgeting, building an emergency fund, investing, and planning for retirement.

Budgeting to Maximise Savings

The first step in working out how much you should save each month is understanding your income and expenses.

A detailed budget acts as a financial guide, showing you where you can afford to cut back.

This isn’t just about skipping the morning Pret a Manger coffee, but extends to making smarter decisions with larger financial obligations like mortgage repayments or car finance.

With a better understanding of your spending habits, you can set a realistic savings target. If £200 aligns well with your budget, then it’s a good starting point as overtime your cash savings will grow if you’re consistent.

Do You Have an Emergency Fund?

Having an emergency fund is essential, no matter your financial status. This acts as a safety net for unforeseen events like sudden job loss or medical emergencies.

Financial experts generally recommend setting aside at least three to six months’ worth of living expenses.

If you’re starting from scratch, prioritising this fund might be a good initial goal before diverting money to other savings or investments.

- Sammie's Hot Tip 🌶️

Start with one month and then build it up with consistent saving to the 3-6 months. Saving money towards an emergency fund is not on everyone’s list but change your thinking and get it moved up to the top.

Investment Opportunities

Investing plays a crucial role in your overall financial strategy, but it’s different from savings.

While the aim of saving is to preserve and have money readily available, investing is about growing your money over the long term.

The power of compound interest means that even modest, regular investments like £200 a month can amass into a considerable sum over the years.

Investing in the stock market will come with its risks but learning how to manage your risk is vital and the stock market can be a wonderful vehicle to build financial security. But, you need to have a long-term mindset.

If you’re new to the investment scene, consider starting with low-risk vehicles like bonds or index funds.

Consider using a stocks and shares ISA so you can build wealth completely tax free.

Watch our video on Index Fund Investing just below.

Planning for Retirement

Although retirement may seem a long way off, early planning is crucial.

Workplace pension schemes, especially those that match your contributions, are an excellent way to prepare for your future.

If you can, try to contribute enough to claim the maximum employer match which is essentially free money. Remember pension plans are a long-term commitment, and you can’t withdraw your pension unless critically ill before the age of 57.

If you’re self-employed, lack access to a company pension or want to grow you pension outside of your workplace pension you might want to consider setting up a personal pension.

The State Of Savings In The UK

The average amount saved by age differs vastly based on age group. According to savings statistics from the ONS, this is how each age group is stacking up:

- 18 to 24-year-olds – £2,481

- 25 to 34-year-olds – £3,544

- 35 to 44-year-olds – £5,995

- 45 to 54-year-olds – £11, 013

- 55 to 64-year-olds – £20,028

- 65 to 74-year-olds – £113, 600

So in just one year, saving £200 a month you’d almost have more in savings than most 18-24-year-olds!

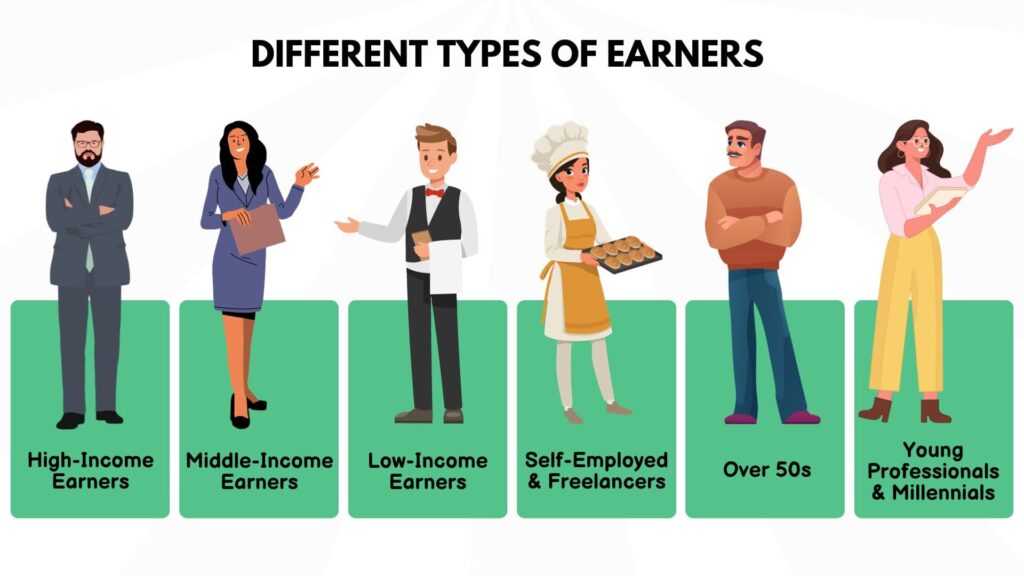

Let’s explore some scenarios where £200 a month could make a difference, depending on your income level or job role.

Contextualising £200 in Various Scenarios

Let’s explore some scenarios where £200 a month could make a difference, depending on your income level or job role.

High-Income Earners

For those raking in a six-figure salary, £200 might seem like a trivial amount. However, even smaller sums can grow thanks to the power of compound interest.

High-income earners frequently have significant outgoings like larger mortgages, school fees, and potential debt due to lifestyle inflation.

Consistently saving £200 each month can serve as a financial buffer and offer room for investment diversification.

Financial planners often suggest high earners should be saving even more, perhaps around £1,000 to £1,500 per month.

Middle-Income Earners

If you’re on an average income, £200 per month is often a more manageable amount that still promises meaningful long-term gains.

Life events like marriage, having children, or career changes can alter your financial landscape. Regularly review your savings strategy to see if £200 remains the optimal amount, especially as inflation and living costs rise.

Low-Income Earners

For those at the lower end of the income scale, even £200 can seem ambitious. Yet, smaller, consistent savings are better than none.

A percentage-based approach, rather than a fixed sum, may be more practical. Government schemes aimed at supporting low-income earners can also be helpful.

The Self-Employed and Freelancers

In the ever-expanding gig economy, having a savings cushion is doubly vital. £200 per month may be achievable in a profitable month but challenging during quieter periods.

A flexible savings strategy, allowing for greater contributions in good months, can provide a buffer for leaner times.

The Over 50s

If you’re over 50 and haven’t been saving consistently, setting aside £200 each month can serve as a strong financial initiative. As retirement approaches, now is an excellent time to fortify your financial reserves.

Utilise financial tools like catch-up contributions to pension schemes to maximise your savings potential.

Young Professionals and Millennials

Compound interest is particularly beneficial for younger savers, even when starting with smaller sums like £200.

While this amount might initially feel steep, especially early in your career, it becomes more realistic as you progress and your salary increases.

MORE LIKE THIS

Conclusion

The world of personal finance can sometimes appear complex and overwhelming, but one element remains essential: a strong savings account.

By setting aside £200 each month, or an amount that’s tailored to your financial circumstances, you’re not just hoarding cash—you’re investing in a future that’s more financially secure and stable.

From learning how to save money to building a dependable emergency fund to seizing varied investment opportunities, even a modest but consistent monthly saving can make a significant contribution to long-term financial well-being.

So, whether you’re at the beginning of your savings journey or looking to refine your existing strategy, never underestimate the potent impact of regularly saving a fraction of your monthly income.

Financial stability might seem like a far-off target, but with a considered approach and a disciplined saving routine, it becomes an attainable reality.

Share on social media

Disclaimer: Content on this page is for informational purposes and does not constitute financial advice. Always do your own research before making a financially related decision.