Sammie Ellard-King

I’m Sammie, a money expert and business owner passionate about helping you take control of your wallet. My mission with Up the Gains is to create a safe space to help improve your finances, cut your costs and make you feel good while doing it.

Having a fixed-term contract for employment can sometimes make it more challenging to secure a mortgage. However, it is not impossible.

In this article, we will explore the options available for individuals who are on a fixed-term contract and looking to get a mortgage.

We will discuss the requirements, and potential challenges, and provide some useful tips for navigating this process successfully.

KEY TAKEAWAYS

Yes, You Can Get a Mortgage on a Fixed-Term Contract: It’s challenging but not impossible, especially if you have a stable employment history and a good credit score.

Boost Your Chances with a Larger Deposit: In the UK, saving a larger deposit can offset the perceived risk associated with a fixed-term contract and improve your mortgage options.

Consult a Specialist: A mortgage advisor or broker familiar with the UK market can navigate the complexities and connect you with lenders more open to fixed-term contracts.

Table of Contents

Boon Brokers are one of the UKs leading online mortgage brokers. They have a 5-star excellent Trustpilot rating with over 543 reviews.

- No mortgage fees

- Whole of market access

- Free online consultations

- Directly authorised by the FCA

- No in person meet ups

Can You Get a Mortgage on a Fixed-Term Contract - The Short Answer

Yes, you can get a mortgage on a fixed-term contract in the UK. While it may be more challenging due to lenders’ preference for stable, long-term employment, it’s far from impossible.

Key factors that can tip the scales in your favour include a strong credit score, a sizable deposit, and a stable employment history.

Understanding the Basics of a Fixed Term Contract

Before diving into the specifics of getting a mortgage on a fixed-term contract, it is important to understand what a fixed-term contract entails.

A fixed-term contract is a type of employment agreement where both the employer and the employee agree on a specific end date for the contract.

This is different from permanent employment, where there is no predetermined end date. Some lenders view you as a temporary worker with a temporary contract, which makes it harder so the length and quality of the contract will make a big difference.

There are many industries where fixed-term contracts like this are in place most prominent in areas like construction where you’ll be working on a project for 12-18 months.

- Sammie’s Hot Tip

If you’re on a fixed-term contract in the UK, consider gathering evidence of contract renewals or consistent employment in your field. This can significantly bolster your mortgage application.

Lenders are more likely to see you as a low-risk applicant if you can demonstrate a history of contract renewals or a steady income in your line of work.

The Challenges of Getting a Mortgage on a Fixed Term Contract

Getting a mortgage on a fixed-term contract can be more challenging because lenders typically prefer stability and steady income when considering mortgage applications.

Here are some of the challenges you might face when trying to get fixed-term contract mortgages:

1. Income Verification

One of the primary concerns for mortgage providers is verifying your income. Since fixed term contracts have an end date, lenders may be worried about the stability of your income and your ability to make mortgage payments.

They want to ensure that you have a consistent source of income throughout the duration of the mortgage. Get things ready like your P60 and payslips.

2. Employment History

Lenders also consider your employment history when assessing your mortgage application. They want to see a stable and consistent employment record alongside your current contract.

Having a series of fixed-term contracts without a permanent position may raise concerns for lenders, as it may indicate a lack of job security.

3. Creditworthiness

Creditworthiness is another important factor that lenders consider. They want to ensure that you have a good credit history and are financially responsible.

A poor credit score may make it more challenging to secure a mortgage, regardless of your employment type.

What Happens If I My Contract finishes in the next 6-12 months?

If your fixed-term contract is due to expire in the next 6-12 months, securing a mortgage could be more challenging. Lenders will want assurance that your contract is likely to be renewed or that you have other employment opportunities lined up.

Some lenders may require a letter from your current employer indicating the likelihood of contract renewal.

If your contract is not renewed, you’ll need to inform the lender, who may reassess your mortgage terms based on your new employment situation.

Boon Brokers are one of the UKs leading online mortgage brokers. They have a 5-star excellent Trustpilot rating with over 543 reviews.

- No mortgage fees

- Whole of market access

- Free online consultations

- Directly authorised by the FCA

- No in person meet ups

Options for Getting a Mortgage on a Fixed Term Contract

While it may be more difficult to get a mortgage on a fixed term contract, it is not impossible. Here are some options you can explore:

1. Saving a Larger Deposit

Saving a larger house deposit can help demonstrate your financial stability and commitment to homeownership. A bigger deposit can also reduce the loan-to-value ratio, which is beneficial when applying for a mortgage.

2. Improve Your Credit Score

Take steps to improve your credit score before applying for a mortgage. Pay your bills on time, reduce any outstanding debts, and avoid applying for new credit in the months leading up to your mortgage application.

3. Seek the Services of a Mortgage Broker

A mortgage broker can help navigate the complexities of getting a mortgage on a fixed-term contract. They have access to a wide range of lenders and can provide advice tailored to your specific situation.

4. Demonstrate a Steady Income

Even though your contract has an end date, you can still demonstrate a steady income by providing evidence of future employment prospects. If you have a track record of securing fixed-term contracts consistently, this can work in your favour.

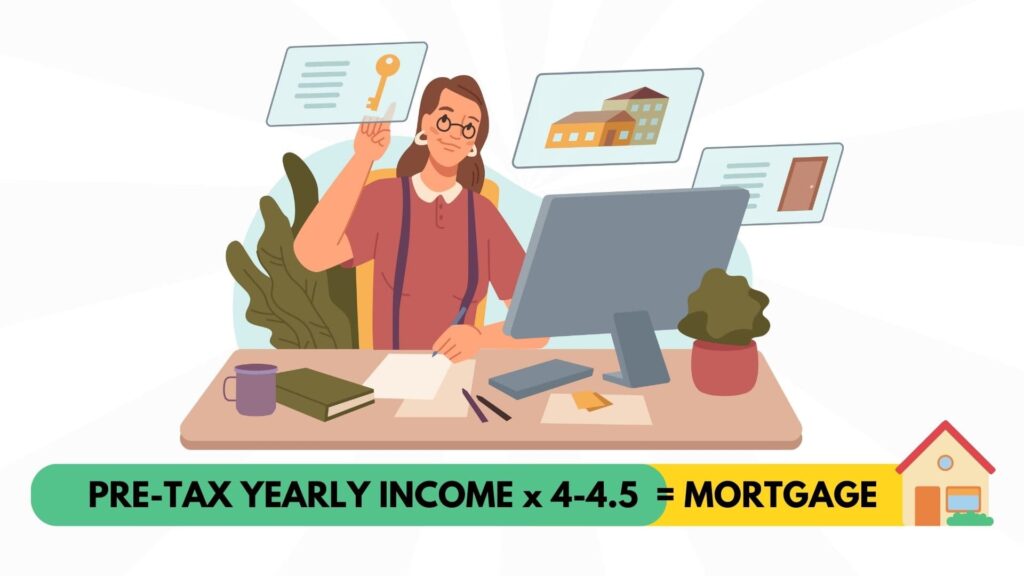

How Much Can You Borrow?

In the UK, the amount you can borrow for a mortgage is generally determined by your income and outgoings, among other factors.

For those on a fixed-term contract, lenders may also consider the duration of the contract and the likelihood of it being renewed.

Typically, you can borrow up to 4.5 times your annual income, although some lenders may offer more or less depending on your circumstances.

It’s essential to use a mortgage calculator to get a more accurate estimate.

Eligibility Criteria

The eligibility criteria for securing a mortgage on a fixed-term contract in the UK can vary among lenders.

However, common requirements include:

- Proof of Income: Payslips, tax returns, and bank statements are usually required.

- Length of Contract: Many lenders prefer contracts that have at least six months remaining. Some may require a history of renewals.

- Employment History: A stable employment history, even with different employers, can be beneficial.

- Credit Score: A good credit score is crucial. In the UK, you can check your credit score through agencies like Experian, Equifax, or TransUnion.

- Deposit: A larger deposit can often offset the perceived risk associated with a fixed-term contract. In the UK, the minimum deposit is usually around 5-10% of the property’s value.

Which Lenders Will Accept Fixed-Term Contracts?

High-street banks like Barclays, HSBC, and NatWest may offer mortgages to those on fixed-term contracts, but their criteria can be stringent.

Specialist lenders and building societies are often more flexible and may offer products specifically designed for fixed-term contractors. It’s advisable to consult a mortgage broker familiar with the UK market for tailored advice.

What about if I'm an agency worker?

If you’re an agency worker, you might be wondering how this affects your mortgage prospects.

The good news is that many lenders are becoming more flexible in their criteria, acknowledging the changing nature of employment and temporary contracts.

However, there are some additional considerations:

- Consistency is Key: Lenders will look for a consistent work history, even if it’s through an agency. A track record of regular assignments can demonstrate income stability.

- Length of Service: The longer you’ve been with an agency, the better. Lenders often like to see at least 12 months of continuous employment, although some may accept less.

- Proof of Income: You’ll need to provide payslips, usually for the past 3-6 months, and possibly a work contract. Some lenders may also request a letter from the agency confirming your employment status and income.

- Type of Work: The sector you work in can also impact your mortgage options. Some sectors are viewed as more stable than others, which could work in your favour.

- Mortgage Broker: Given the complexities, consulting a mortgage broker familiar with the UK market and the specific challenges faced by agency workers can be invaluable.

Boon Brokers are one of the UKs leading online mortgage brokers. They have a 5-star excellent Trustpilot rating with over 543 reviews.

- No mortgage fees

- Whole of market access

- Free online consultations

- Directly authorised by the FCA

- No in person meet ups

FAQs

Here are some frequently asked questions about getting a mortgage on a fixed-term contract:

Can I get a mortgage on a fixed-term contract if my contract is expiring within the next few months?

While it may be more challenging, it is still possible to get a mortgage if your contract is expiring soon.

Lenders will consider factors such as your employment history, income stability, and future employment prospects before making a decision.

Will my credit score impact my chances of getting a mortgage on a fixed-term contract?

Yes, your credit score will play a significant role in getting a mortgage. Lenders want to ensure that you have a good credit history and are financially responsible.

It is advisable to work on improving your credit score before applying for a mortgage.

Should I approach a mortgage lender directly or use a mortgage broker?

Both options have their pros and cons. Approaching a mortgage lender directly allows you to explore their specific requirements and offerings.

On the other hand, a mortgage broker can provide access to multiple lenders and provide personalised advice based on your situation.

What documents do I need to provide when applying for a mortgage on a fixed-term contract?

When applying for a mortgage on a fixed-term contract, you will typically need to provide documents such as proof of income, employment contract, bank statements, identification documents, and details of your credit history.

Is it possible to get a mortgage on a fixed term contract if I have a gap in my employment history?

Having a gap in your employment history can make it more challenging to secure a mortgage. However, each lender has different criteria, and some may be more lenient than others.

It is advisable to discuss your specific situation with a mortgage broker or lender directly.

Conclusion

Securing a mortgage on a fixed term contract may require some additional effort and planning, but it is not impossible.

By understanding the requirements, addressing potential challenges, and exploring all available options, you can increase your chances of successfully obtaining a mortgage. Remember to seek professional advice, consider improving your credit score, and demonstrate your financial stability to lenders.

With careful planning and preparation, you can achieve your dream of homeownership, even with a fixed term contract.”

Share on social media

Disclaimer: Content on this page is for informational purposes and does not constitute financial advice. Always do your own research before making a financially related decision.