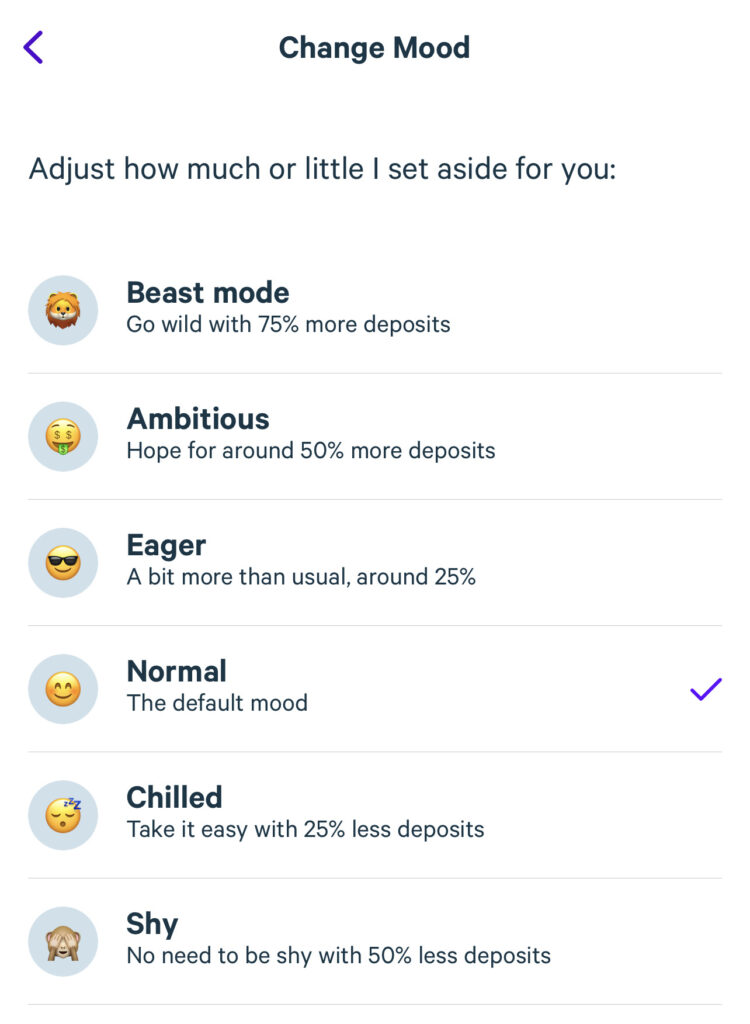

What an app! I utilise their smart AI to set money aside automatically every payday!

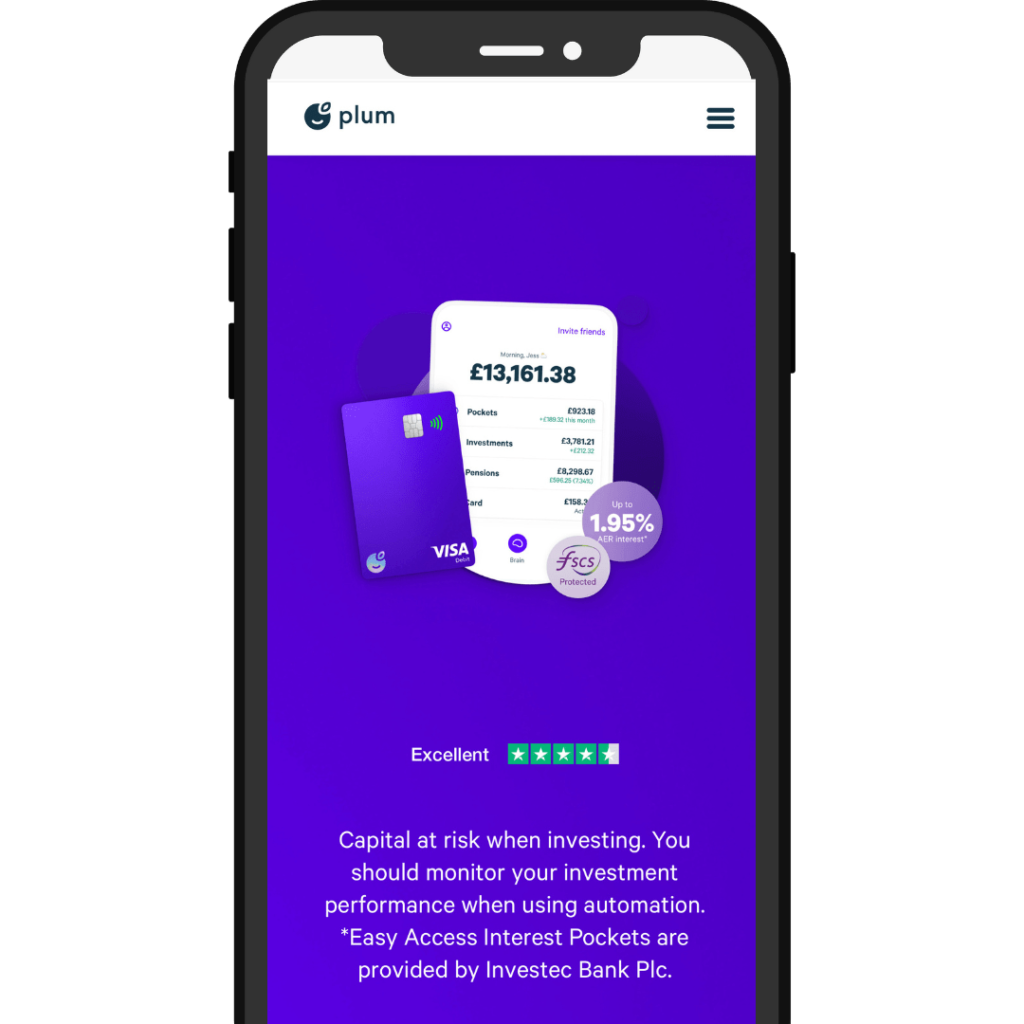

You can earn up to 3.63% AER with their Easy Access Interest Pocket, and begin investing in up to 3000 stocks and funds from as little as £1.

- Auto save and invest

- Savings pots with interest

- Low fees in comparison to Chip

- ISAs, SIPPs and savings accounts available

- Easy to use mobile app

- Best saving interest rates hidden behind paywalls

- Tiered fee levels to access all investment options

Our Rating

- Suitable For Beginners

- Useful Features

- User Experience

- Price / Fees

- Customer Feedback

- Customer Service

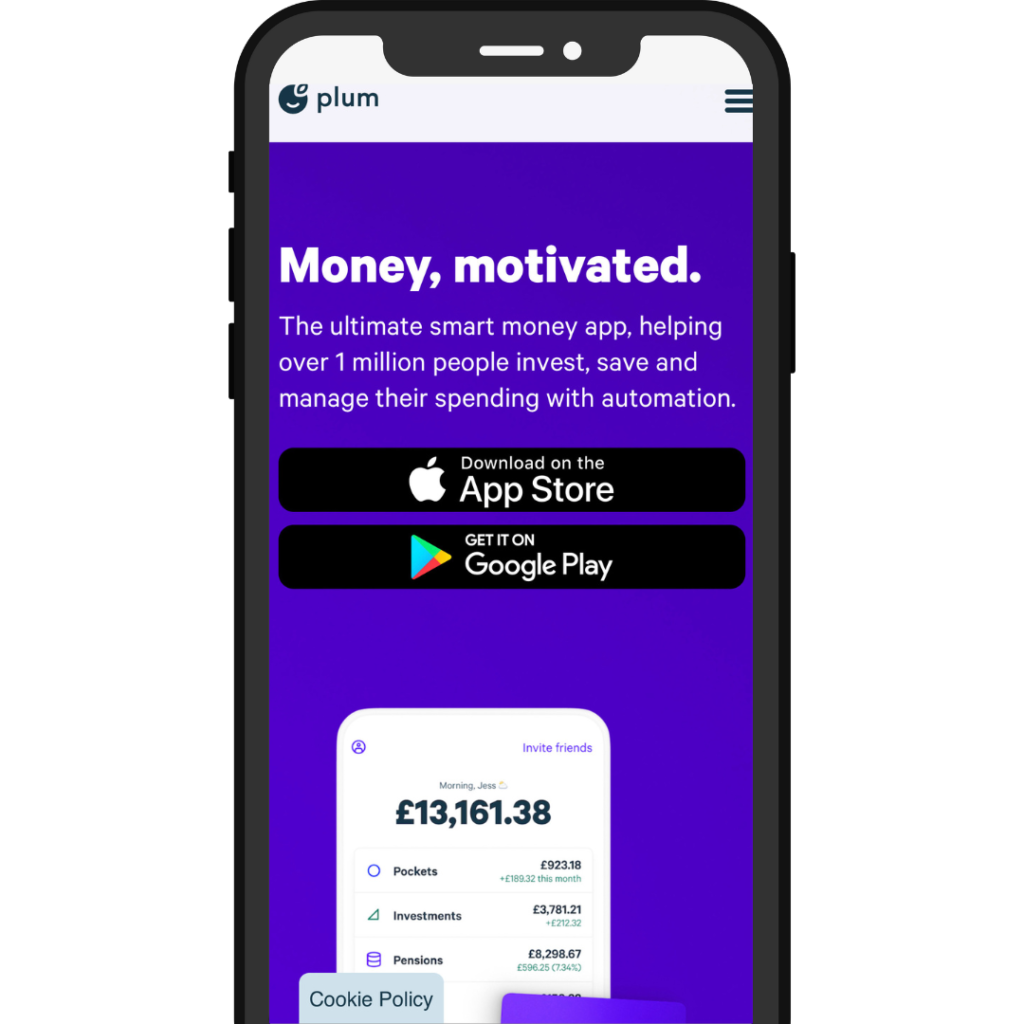

Plum is the award-wining ultimate smart money app, helping over 1 million people to invest, save and manage their spending with automation.

I'm personally using the app as part of my savings plan and absolutely love their automatic saving features.

What an app! I utilise their smart AI to set money aside automatically every payday!

You can earn up to 3.63% AER with their Easy Access Interest Pocket, and begin investing in up to 3000 stocks and funds from as little as £1.

- Auto save and invest

- Savings pots with interest

- Low fees in comparison to Chip

- ISAs, SIPPs and savings accounts available

- Easy to use mobile app

- Best saving interest rates hidden behind paywalls

- Tiered fee levels to access all investment options

Plum is the award-wining ultimate smart money app, helping over 1 million people to invest, save and manage their spending with automation.

I'm personally using the app as part of my savings plan and absolutely love their automatic saving features.

What an app! I utilise their smart AI to set money aside automatically every payday!

You can earn up to 3.63% AER with their Easy Access Interest Pocket, and begin investing in up to 3000 stocks and funds from as little as £1.

- Auto save and invest

- Savings pots with interest

- Low fees in comparison to Chip

- ISAs, SIPPs and savings accounts available

- Easy to use mobile app

- Best saving interest rates hidden behind paywalls

- Tiered fee levels to access all investment options