Sammie Ellard-King

I’m Sammie, a money expert and business owner passionate about helping you take control of your wallet. My mission with Up the Gains is to create a safe space to help improve your finances, cut your costs and make you feel good while doing it.

I’m self-employed and have gone through this exact process in the last 6 months.

Let me tell you, remortgaging when self-employed is totally doable, but there are some differences to what might be considered a normal remortgage.

There are certain challenges that the mortgage application might throw at you, but it’s my job to ensure you’re prepared for this, so when you call up your mortgage advisor, he’s shocked you know it all already!

Now I want to give you everything you need to know about how to remortgage when self-employed and how you can potentially secure a better mortgage deal.

Key Takeaways:

- Remortgaging as a self-employed individual is achievable with proper planning, and it can offer benefits like better rates and equity release.

- Lenders generally look for 2-3 years of accounts or tax returns for self-employed applicants, making income stability and credit score key factors for a successful remortgage.

- Utilising a mortgage broker specialising in self-employed cases can help you navigate the complexities and secure the best mortgage deal.

Table of Contents

Remortgage when self-employed

Remortgaging when self-employed is the process of switching your existing mortgage to a new deal, either with the same lender or a different one.

It can be a beneficial option for self-employed individuals who want to take advantage of better rates or release equity from their property.

For example, I remortgaged from the help-to-buy scheme which meant I released equity to clear the 20% government loan I was given as support. This meant my terms were renegotiated and I then owned 100% of the property.

And yes, it was different and the process required planning and preparation, as lenders often assess self-employed income differently from traditional employment.

Something to note is that remortgaging at the end of a fixed term can be done 6 months out so get yourself ready if that’s what you’re considering.

Boon Brokers are one of the UKs leading online mortgage brokers. They have a 5-star excellent Trustpilot rating with over 543 reviews.

- No mortgage fees

- Whole of market access

- Free online consultations

- Directly authorised by the FCA

- No in person meet ups

Here are some key questions you should ask yourself before you apply.

1. Were you already self-employed when applying for a mortgage?

If you were that’s a good thing as you’ll understand the process and lenders will be more favourable to your application.

They’ll do all of the same checks credit score, paperwork etc but you should be able to get through this much easier.

2. You weren’t self-employed when you got your current mortgage?

This is completely normal and many people decide to start their own business or go and work for themselves instead of a corporate job.

In this case, lenders prefer you to have at least two years of company-filled accounts.

There are cases where lenders will look at 1 year’s worth of accounts but this means the pool is smaller meaning your deal could be worse.

Equally important is the amount you are earning. If you’re earning more then you may be able to borrow a larger amount but if your income has gone down since you were self-employed you need to factor this in.

Calculate how much you can afford for a self employed remortgage with our mortgage calculator.

3. What about if I’m newly self-employed?

A newly self-employed mortgage is a little tougher to get. I mentioned just above lenders want to see a minimum of 1 but ideally 2-3 years’ worth of company accounts.

However, not all is lost and you won’t be left without a mortgage. You can move onto a variable rate with your current lender but this is obviously subject to change with the interest rates moving up and down.

Or you can product transfer directly with your current lender as they have already completed all their checks on you. This does mean you’ll need to take the deal you are offered but allows you to get onto new terms.

4. Differences between a sole trader and a company director when getting a mortgage?

If you own more than 20-25% of a business, lenders usually consider you self-employed.

Whether you’re a sole trader or a limited company director, expect to show 2-3 years of full accounts or SA302s for remortgaging. Limited company directors, be prepared to also prove dividends and retained profits.

Watch out if you keep a low salary to save on National Insurance and tax; it can make your income appear lower than it is.

Some lenders don’t factor in retained profits, so if you hold back a chunk of earnings in the business, aim for a lender who gets this. They’re more likely to offer you a more generous mortgage.

Boon Brokers are one of the UKs leading online mortgage brokers. They have a 5-star excellent Trustpilot rating with over 543 reviews.

- No mortgage fees

- Whole of market access

- Free online consultations

- Directly authorised by the FCA

- No in person meet ups

Key factors to consider when remortgaging as a self-employed individual

The key factors to consider are as follows:

1. Lenders' Requirements for Self-Employed Borrowers

Lenders have specific criteria for self-employed borrowers due to the unpredictable nature of their income.

These criteria often include:

- Proof of income: Lenders generally require two to three years’ worth of accounts or self-assessment tax returns to verify your income.

- Continuity of income: Lenders will look at the consistency and stability of your income over a period to assess your reliability.

- Affordability assessment: A thorough evaluation of your income and outgoings will be conducted to determine how affordable the mortgage is for you.

- Credit history: Your credit score will also be taken into consideration during the mortgage application process.

2. Mortgage Options for the Self-Employed

If you’re self-employed, you have several types of mortgages available:

- Self-employed mortgage: This mortgage is specifically tailored for self-employed borrowers, taking their unique income structure into account.

- Contractor mortgage: Those working on a contractual basis, often on short-term projects, might be eligible for a contractor mortgage.

- Professional mortgage: Some professions, like doctors or solicitors, may have access to specialised mortgage packages.

- Buy-to-let mortgage: Self-employed landlords can consider buy-to-let mortgages for investment properties.

3. Benefits of Remortgaging for the Self-Employed

Remortgaging can offer several potential advantages if you’re self-employed:

- Access to better rates: Remortgaging could provide the opportunity to secure a more favourable interest rate, saving you money in the long term.

- Release equity: You could release equity from your home for various uses, such as home improvements, consolidating debts, or business investments.

- Flexible mortgage options: Remortgaging enables you to explore different mortgage deals that might better meet your financial needs.

4. Steps to Remortgage as a Self-Employed Individual

The process to remortgage when self-employed usually involves the following steps:

- Assess your eligibility: First, determine whether you meet the lender’s requirements for a self-employed borrower.

- Gather documentation: Assemble the necessary paperwork, including accounts or self-assessment tax returns, proof of income, and bank statements.

- Seek professional advice: It’s advisable to consult a mortgage broker or financial adviser who specialises in self-employed mortgages.

- Compare mortgage deals: Investigate various mortgage options, comparing interest rates, terms, and fees to identify the most suitable deal.

- Apply for the remortgage: Submit a complete and accurate application to your chosen lender.

- Undergo an affordability assessment: The lender will examine your income, credit score, and other factors to gauge your ability to afford the mortgage.

- Property valuation and legal steps: A property valuation may be arranged, and the legal transfer of the mortgage will commence.

- Complete the remortgage: Upon approval, the remortgage process can be finalised, and you can switch to your new mortgage deal.

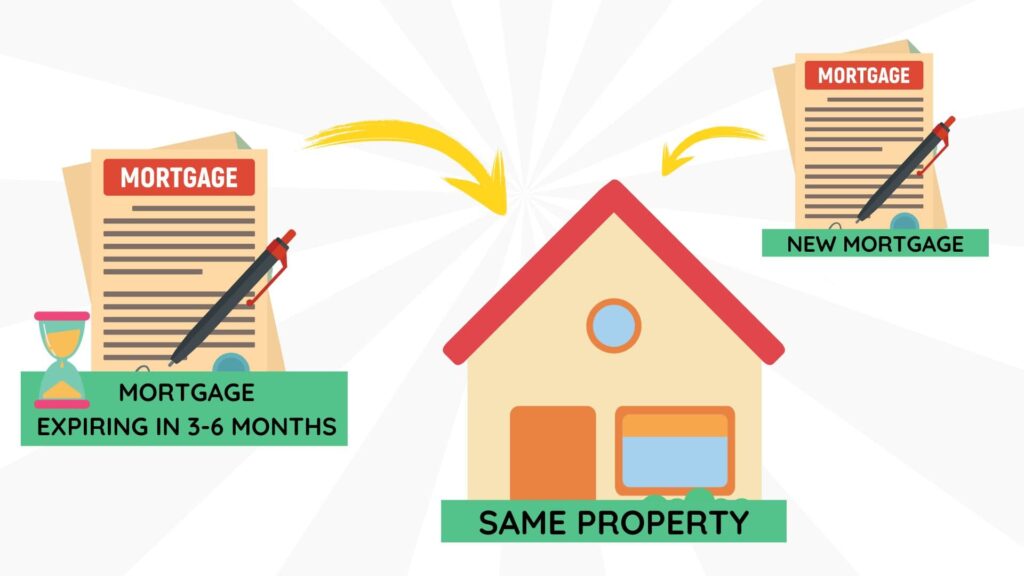

When should you look to remortgage?

Consider remortgaging when you’re nearing the end of your current mortgage deal, usually around 3-6 months before it expires.

This gives you ample time to shop around, compare rates, and complete the remortgage process without slipping onto your lender’s Standard Variable Rate (SVR), which can be higher.

Consider remortgaging if interest rates drop or if you’ve improved your credit score, as you could secure a better deal.

What about if I want to extract equity when remortgaging?

To extract equity requires you to have some built up in the first place.

Perhaps you might be looking to remortgage to build an extension or to invest in a property to make money.

The key here is to inform the lender of your goals and ensure any new terms fit with your financial make up.

In some cases if you’re extrating equity your terms could go back up so do think about this.

How to Get the Best Rates When Remortgaging?

To get the best rates:

Keep your credit score in tip-top shape. A higher score often leads to better rates.

Assess your Loan to Value (LTV) ratio. The lower your LTV, the better the rates you could get.

Gather solid proof of income, especially 2-3 years of accounts or SA302s, to demonstrate financial stability.

Use a mortgage broker who specialises in self-employed cases. They can guide you to lenders who offer competitive rates for your unique income structure.

Compare multiple mortgage products, keeping an eye on rates, fees, and flexibility.

Consider fixing your mortgage rate if interest rates are low or likely to rise, to lock in that rate for a set period.

By planning ahead and paying attention to these factors, you’re well-placed to secure the best rates when remortgaging.

Boon Brokers are one of the UKs leading online mortgage brokers. They have a 5-star excellent Trustpilot rating with over 543 reviews.

- No mortgage fees

- Whole of market access

- Free online consultations

- Directly authorised by the FCA

- No in person meet ups

FAQs

Can I remortgage if I am self-employed?

Yes, it is possible to remortgage if you are self-employed. However, the process may be slightly different compared to traditional employment. Lenders will typically require proof of income, continuity of income, and assess your affordability based on your self-employed earnings.

How many years do I need to be self-employed to remortgage?

Lenders generally require a minimum of two to three years of self-employed accounts or tax returns to assess your income and determine mortgage affordability.

However, some lenders may have specific criteria, so it’s important to check with different lenders or seek professional advice.

Will I get a better mortgage deal as a self-employed individual?

Yes, remortgaging can be a way to release equity from your property.

Depending on the value of your property and the existing mortgage, you may be able to access funds that can be used for various purposes, such as home improvements, debt consolidation, or investment opportunities.

Can I switch to a fixed-rate mortgage if I am self-employed?

Yes, it is generally possible to switch to a fixed-rate mortgage if you are self-employed.

A fixed-rate mortgage offers the benefit of having a stable interest rate for a specific period, which can provide certainty and predictability in your mortgage payments.

What are the potential challenges of remortgaging when self-employed?

Some potential challenges of remortgaging when self-employed include:

- Evidencing income: Lenders may require detailed documentation and evidence of your income, which can be complex for self-employed individuals.

- Affordability assessment: Self-employed income may vary from year to year, which can affect how lenders assess your affordability for the mortgage.

- Limited options: Some lenders may be more cautious when lending to self-employed borrowers, resulting in a narrower range of mortgage deals available.

How can a mortgage broker help me with remortgaging?

A mortgage broker who specialises in self-employed mortgages can provide valuable assistance throughout the remortgaging process.

They can help you identify suitable lenders, navigate the application process, gather the required documentation, and negotiate the best mortgage deal on your behalf.

They can also answer how long will a remortgage take and hold your hand throughout the entire proces.

Conclusion

Remortgaging when self-employed can be a beneficial financial move, providing access to better deals and the potential to release equity.

By understanding the requirements of lenders, exploring available mortgage options, and seeking professional advice, self-employed individuals can navigate the remortgaging process with confidence.

Remember to research, compare rates, and consider the long-term financial implications before making a decision.