If you have found an ISA with a better rate or features that suit you, you can move your money to a new provider without losing its tax-free status. The key is to do it as a transfer rather than a withdrawal.

Transferring an ISA is straightforward once you know the rules, and importantly it does not use up your annual allowance. This guide covers how ISA transfers work, how long they take, the different transfer types, and the changes coming in 2027.

Key Takeaways: Essential Insights on Transferring Your ISA

Maintain Your ISA’s Active Status: Before initiating any transfer, it’s crucial to keep your current ISA open. Closing your ISA prematurely can lead to losing its tax-efficient benefits. We’ll explain how to navigate this to ensure a seamless transfer.

-

Understand Transfer Types: Different ISAs have different transfer rules. Whether you’re moving from a Cash ISA to a Stocks and Shares ISA or vice versa, each type has its nuances. Learn the ins and outs to make an informed decision that aligns with your financial goals.

-

Beware of Transfer Timeframes: Timing is everything. Transferring an ISA isn’t instantaneous and can impact your investment strategy. We’ll delve into typical timeframes and how to plan your finances around these critical periods to avoid potential disruptions in your savings growth.

Table of Contents

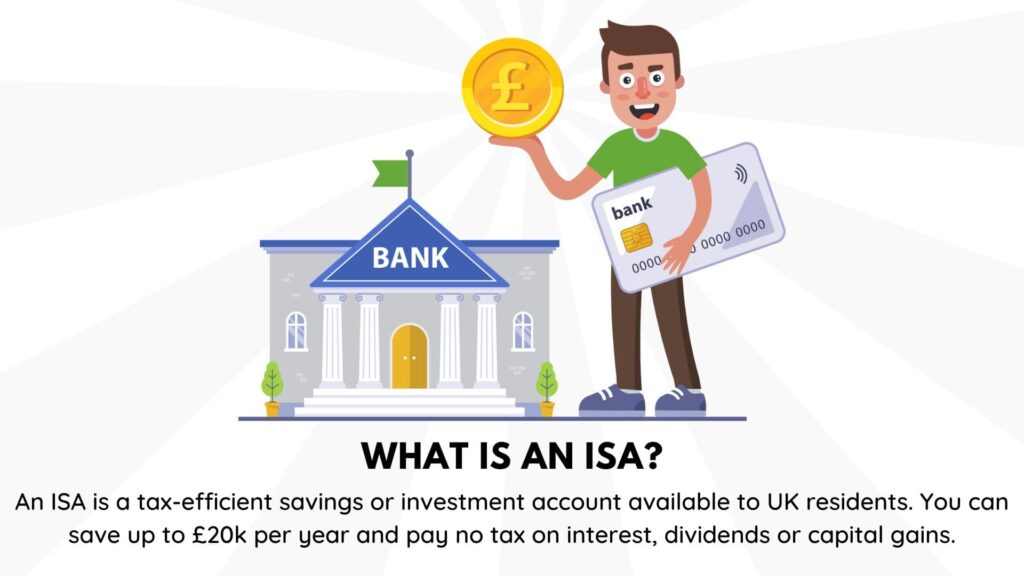

What is an ISA?

An Individual Savings Account (ISA) is a tax-efficient savings or investment account in the UK. It comes in various types:

- Cash ISA: Tax-free savings account.

- Stocks and Shares ISA: Tax-free investment in stocks, shares, and more.

- Innovative Finance ISA: Tax-free investment in peer-to-peer lending, crowdfunding, etc.

- Lifetime ISA: Government bonus for home purchase or retirement savings.

- Junior ISA: Tax-efficient savings for children under 18.

Each tax year, there’s an ISA allowance, dictating the maximum contribution across all ISAs. Contributions don’t affect the Personal Savings Allowance.

Withdrawals are generally allowed without losing tax benefits, with exceptions for Lifetime ISAs.

Recent and Upcoming ISA Changes

- Multiple ISAs of the Same Type: Savers can subscribe to multiple ISAs of the same type within a tax year, within the £20,000 overall ISA limit.

- Exploring Better Deals: This change allows savers to take advantage of different offerings and secure more competitive deals throughout the year.

- Partial Transfers Allowed: Savers can make partial transfers between different ISA providers.

- Boost for Cash ISA Savers: The changes are particularly beneficial for those interested in cash ISAs, offering opportunities to adapt to market conditions.

- Unchanged ISA Allowance: Despite these positives, experts criticise the unchanged overall ISA allowance of £20,000 since 2017, arguing for an increase to reflect inflation.

- Fractional Shares in ISAs: The reforms include the ability to invest in fractional shares within ISAs, ideal for investing in high-value stocks.

From 6 April 2027, more changes are coming (still subject to consultation):

- Smaller cash ISA limit: under-65s will be able to pay up to £12,000 a year into a cash ISA, down from £20,000, although the overall £20,000 ISA allowance stays the same. The full £20,000 cash limit returns from the tax year in which you turn 65.

- A new charge on cash in investment ISAs: a 22% charge will apply to interest earned on cash held in a stocks and shares, Lifetime or innovative finance ISA. Your actual investments and money market funds are exempt.

- A transfer restriction: under-65s will not be able to transfer money from a non-cash ISA (such as a stocks and shares ISA) into a cash ISA. The reverse is still allowed, and the restriction lifts from the tax year you turn 65.

Always keep your ISA open!

It is important to not close the ISA you want to transfer. If you do, you are losing that tax-free protective bubble around your money and may start eating into your annual ISA allowance.

By keeping your ISA open, it can be transferred without issues and without affecting this year’s annual allowance.

If you transfer a £10k ISA, you’ll still have a £20k allowance this year. The same goes if you transfer £25k or £47,500. If you withdraw it by closing the ISA and you want to put it into another ISA, you’ll use £10k of that £20k allowance.

If you have more than £20k, you won’t be able to put it all back into an ISA. This is why keeping your account open and going down the transfer route is important.

In short, be sure you don’t opt to close it and get your money because if you then want to put it back into another ISA, you’ll have to use your allowance.

Meaning you can’t take advantage of more tax-free savings this year. Transferring does not count toward your annual ISA allowance.

How to transfer an ISA?

Of course, you need to be able to transfer your ISA should you want to. In order to do this the right way, you need to get in touch with the ISA provider you want to move to.

Then fill in an ISA transfer form so your account can be moved.

For cash ISAs, your transfer should complete in no more than 15 days. For all other types of ISA, you are looking at no longer than 30 days for your transfer to finalise.

You’ll need to familiarise yourself with the ISA transfer rules of your provider.

If your transfer is taking longer than expected, your first port of call should be your ISA provider. If you are unhappy for any reason, you can contact the Financial Ombudsman Service.

Does transferring an ISA count as opening a new one?

Transferring an ISA does not count as opening a new one in the context of the ISA subscription rules in the UK. When you transfer an ISA, you’re essentially moving the funds from one ISA to another, either with the same or a different provider.

This process does not affect your annual ISA subscription limit, as you’re not contributing new money, but rather moving existing funds within the ISA framework.

Can I transfer between different types of ISA?

Cash ISA to Stocks and Shares ISA

When transferring from a Cash ISA to a Stocks and Shares ISA, you’re moving from a secure, interest-based saving scheme to one involving stock market investments.

This exposes your savings to higher risks and potential rewards. Evaluating your risk tolerance and investment objectives is key before initiating this transfer.

Stocks and Shares ISA to Cash ISA

Transferring from a Stocks and Shares ISA to a Cash ISA involves moving funds from volatile investments to a stable, interest-earning account.

This transfer is often considered by those looking for reduced risk, particularly in scenarios like approaching retirement or needing guaranteed access to funds.

Note: from April 2027, under-65s will no longer be able to make this particular move, as transfers from a non-cash ISA into a cash ISA are being restricted. The reverse (cash into investments) is still allowed, and the restriction lifts from the tax year you turn 65.

Transferring into a Lifetime ISA

Moving other ISA types into a Lifetime ISA is relatively straightforward, offering a strategic way to save for a first home or retirement. Be mindful of the LISA’s annual contribution cap and its contribution towards your total ISA limit.

Transferring out of a Lifetime ISA

Transferring out of a Lifetime ISA can be complex and potentially disadvantageous due to penalties.

Withdrawing funds for reasons other than buying your first home or reaching age 60 incurs significant penalties, including the loss of the government bonus and a part of your savings.

Transferring Junior ISAs

Transferring between Junior Cash ISAs and Junior Stocks and Shares ISAs offers flexibility in switching between saving and investing strategies as the child’s financial situation or market conditions evolve. Remember, the funds in a Junior ISA are locked until the child turns 18.

In each case, ensure the transfer is executed correctly through the ISA providers to maintain the ISA’s tax-efficient status.

Also, consider any applicable fees or charges and the timing of your transfer, especially for Stocks and Shares ISAs, to navigate market fluctuations effectively.

Can I transfer more than one ISA?

You can transfer more than one ISA into a different ISA account. You can quickly lose track if you have an array of ISA scattered around. Perhaps you have one you forgot you even opened and paid into!

This is often called consolidating your ISAs and bringing them together in one pot.

The only thing to ask yourself is protection. The FSCS protects you up to £120k per banking institution, not per bank account.

That means if you have a lot of money in your ISAs, you still might want them with separate providers due to this financial protection.

For example, it’s best to split £150k of ISA investment into two ISAs, rather than putting it into one and risking that £30k. We go into this some more when talking about stocks and shares ISAs and how many can you have.

Can you transfer money from an ISA to a current account?

Yes, you can transfer money from an ISA to a current account. This process is fairly straightforward, but there are a few key points to consider:

- Withdrawal Process: You can transfer money from an ISA to a current account via online banking, phone, or in-branch.

- ISA Allowance Impact: Withdrawing doesn’t affect your annual ISA limit, but re-depositing counts towards it.

- Flexible ISA Terms: Some ISAs let you withdraw and replace funds within the same tax year without impacting your limit.

- Lifetime ISA Charges: Withdrawing from a Lifetime ISA before age 60 for non-qualifying reasons incurs a charge and loss of the government bonus.

- Tax Implications: Once withdrawn, funds lose their tax-free status, and any future gains may be taxable.

Remember, always check the specific terms of your ISA for any restrictions or charges.

Reason to transfer an ISA

You might want to move your ISA to another provider for many reasons like:

- You are unimpressed with the performance of your ISA.

- Your friend is performing well with their provider and you want to join them

- You opened your CASH ISA many years ago and better rates are available

- There’s more investment options available at another provider

- The new providers fees have increased and you’re not happy

- There’s cash benefits to switching your ISA

There are lots of reasons why people will look at how to transfer an ISA.

How much can you pay into an ISA?

Remember, you have an annual allowance for ISA contributions. This is £20,000. When the tax year is up, you will lose any allowance you haven’t put in, and the allowance resets for the coming year.

This is why so many people put anything they can afford away into ISAs before the turn of the new tax year. The deadline for that year’s contributions is midnight on 5 April.

You can choose to use your ISA allowance however you want. However, you cannot go over that £20k figure. You can split that allowance across different types of ISAs if you have them.

Since April 2024 you can also pay into more than one ISA of the same type in a tax year, so you could split your cash ISA across two providers if you wanted, as long as your total stays within the £20,000 limit. From 6 April 2027, under-65s will have a lower £12,000 cash ISA limit, though the overall £20,000 allowance is unchanged.

It’s also worth noting that there is a maximum of £4,000 contributions for a Lifetime ISA.

An example of how you could use your allowance is like this. You put the maximum of £4000 into a Lifetime ISA, add £6000 to your cash ISA and then put £10k into a stocks and shares ISA.

Of course, if you could only put £4k, £6k and £9k away, the £1000 allowance left over would vanish when the tax year ends.

The ISA limit for Junior ISAs is £9,000.

Can you transfer shares into ISAs?

Yes, you can transfer shares into an ISA, but there are specific rules and limitations to consider. This process is typically known as a “Bed and ISA” transaction. Here’s how it works:

Sell and Re-buy: You sell the shares outside of your ISA and then immediately re-buy them within your Stocks and Shares ISA. This process realises any capital gains or losses on the shares and uses your annual ISA subscription limit.

Capital Gains Tax Consideration: If the sale of your shares generates a capital gain, it may be subject to Capital Gains Tax if it exceeds your annual exempt amount. However, once the shares are within your ISA, any future gains will be free from Capital Gains Tax.

ISA Subscription Limit: The amount you re-invest in your ISA counts towards your annual ISA subscription limit. For the 2026/27 tax year, this limit is £20,000.

Employee Shares: If you have shares from an employee share scheme, you might be able to transfer these directly into a Stocks and Shares ISA without selling them first, under certain conditions.

It’s important to note that you cannot transfer shares directly into an ISA without selling and re-buying them, except for shares from certain types of employee share schemes.

No. Transferring an existing ISA from one provider to another does not count towards your annual £20,000 allowance, because you are moving money you have already paid in rather than adding new money. Only new contributions use your allowance.

A cash ISA transfer should complete within 15 working days, and other types of ISA within 30 days. If it takes longer, contact your new provider first, and you can escalate to the Financial Ombudsman Service if needed.

Yes, you can transfer an ISA whenever you like, and as often as you like. If you are moving money you have paid in during the current tax year you usually have to transfer all of it, while money from previous years can be moved in full or in part.

Yes. You can transfer a Lifetime ISA to another Lifetime ISA provider without penalty. Transferring it to a different type of ISA, or withdrawing before age 60 for anything other than a first home, triggers the 25% government charge. You cannot transfer an ISA into someone else’s name.

Final Thoughts

If it’s been some time since you opened your ISA, it is well worth looking at other products that have come to market since. You might see that your money is only making 2%, whereas a higher percentage might be available.

Being able to easily transfer your ISA to take advantage of that better rate is key. Now you know how to transfer an ISA, it’ll be a breeze.

Share this article with friends

Disclaimer: Content on this page is for informational purposes and does not constitute financial advice. Always do your own research before making a financially related decision.