There is no outright winner. Both are excellent tax wrappers, and the right choice comes down to when you will need the money.

As a rule of thumb: use an ISA for short and medium-term goals, and a SIPP for your retirement pot.

Both a SIPP and an ISA hand you tax breaks that an ordinary account cannot. The real question is which one to feed first, so let’s break them down.

Table of Contents

SIPP vs ISA

Both accounts charge zero capital gains tax on any profit or interest you make.

The main difference is access: a SIPP is locked until retirement age, whereas an ISA stays flexible and can be withdrawn at any time.

If you are familiar with US retirement accounts, the ISA is the closest Roth IRA UK equivalent, while a SIPP works more like a Traditional IRA.

| Feature | SIPP (pension) | Stocks & Shares ISA |

|---|---|---|

| Upfront tax relief | 20% basic rate, 40% higher rate, 45% additional rate | None (you pay in from taxed income) |

| When can you access it? | Locked until age 55 (57 from April 2028) | Anytime, with no penalty |

| Tax on withdrawal | 25% tax-free, the rest taxed as income | 100% tax-free |

| Annual allowance (2026/27) | £60,000, or 100% of your earnings if lower | £20,000 |

| Tax on growth | No capital gains or dividend tax | No capital gains or dividend tax |

| Best for | Long-term retirement savings | Flexible goals and bridging early retirement |

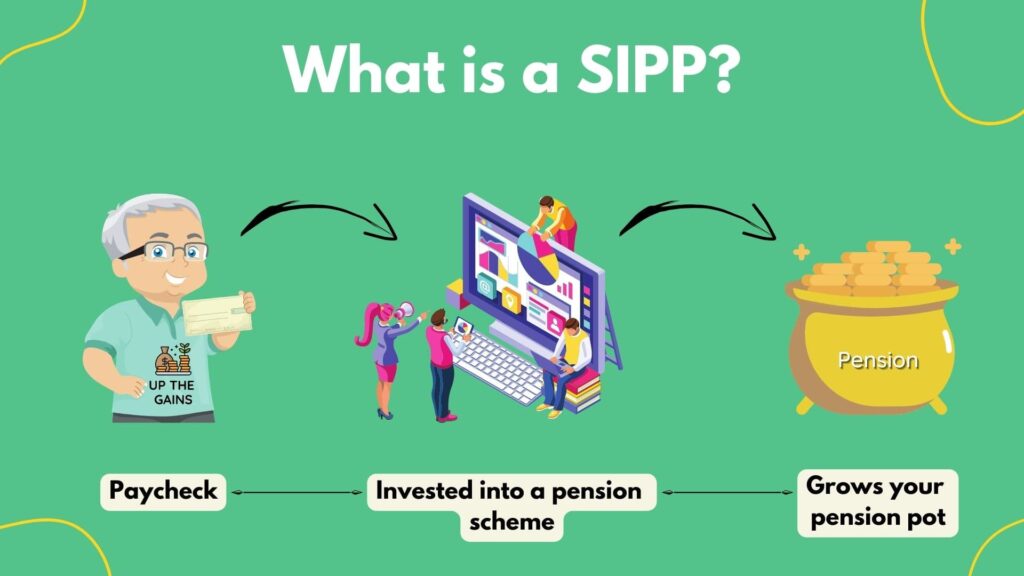

What is a SIPP?

A SIPP or self-invested personal pension allows you to choose exactly where your money is invested.

Essentially you have complete autonomy over the types of investments you hold, allowing you access to a range of shares, funds and trusts.

Personal or private pensions, as they can also be known, are different from your workplace pensions which your company will provide for you.

Company pensions in the UK are usually with a provider like Nest or People’s Pension, and whilst these companies are market leaders, you have little say over where your money is going.

I have a company pension, which I pay myself through Up the Gains, and I invest some of my ‘wages’ into a SIPP.

The key is to maximise your money as the state pension of £241.30 a week is nowhere near enough for most of us to live on once we get to retirement. Having that extra cushion of a pension will take the stress away.

The key benefits of a SIPP:

- Freedom to choose where your money is going

- Expert-managed options where trusted managers will invest your money for you.

- Not subject to pay income tax and capital gains tax from growth and interest

- Exempt from inheritance tax

- You can have multiple SIPPs

- You can pay £60,000 each year or 100% of your salary into your SIPP – whatever number is lower

- Get a government bonus (20%) on everything you put in

- If you’re a higher rate taxpayer, you can get 40% back, and this increases to 45% for additional rate taxpayers

SIPP Rules

SIPPs have a specific set amount of rules that benefit the individual that pays in. Let’s take a look, as this is where it gets interesting.

SIPP tax relief

- Pension annual allowance is up to £60,000 or 100% of your salary. This resets each tax year which runs from April to April

- This amount is eligible for the 20% government bonus as a basic rate taxpayer, so for example, if you pay £80, you would have £100 in your personal pension

- You do not need to do anything to get your tax relief, as your pension provider will handle this for you

- If you’re a higher-rate taxpayer, you can claim an additional 20 or 25%, but this would need to be claimed via a self-assessment

- Your extra tax relief as a higher-rate taxpayer is paid back to you by HMRC to a nominated personal bank account

- You can claim back up to four years of higher rate pension tax relief by completing a self-assessment

Is there a limit on the size of my SIPP?

- The Lifetime Allowance was abolished on 6 April 2024, so there is no longer a cap on the total you can build up in a pension.

- Instead, the tax-free cash you can take is capped at £268,275 (the Lump Sum Allowance). Anything above your tax-free portion is taxed as income when you withdraw it.

Drawdown / Withdrawing

Now all these tax benefits sound great, but it’s important to note that you cannot withdraw your pension before the age of 55. This number is set to increase to 57 in April 2028.

You have a few options to consider when taking money out of your pension:

- Lump Sum – you can take up to 25% of your entire pension in a lump sum tax-free

- Regular drawdown payments – You can arrange regular payments, which are classed as income, so you will need to stay below the income tax-free threshold of £12,570, or you’ll be subject to income tax payments

- Multiple Lump Sums – You can take multiple lump sum payments with the first 25% of each payment tax-free and the remaining 75% subject to income tax at the marginal rate

If you need help with what to do when drawing down your pension savings, then speak to your provider or a financial adviser for some professional advice.

Workplace pension or personal pensions?

Workplace pensions do have their benefits due to the legal minimum matched contribution by an employer being a minimum of 3%.

Your employer decides the kind of workplace pension you pay into, but you should look to maximise this as it’s essentially free money. If, for example, your employer contributions go up to 5,6 or even 10%, then pay more into your workplace pension.

Free money is free money.

Then you could have a smaller personal pension which you control to back it up. It depends on how much control you have, what you’re being paid and whether your employer has a good pension scheme.

Want to go deeper on how these pieces fit together? We break it down in our guide to the UK equivalent of a 401(k): the workplace pension and SIPP.

Add this all up, and you could be one step ahead of most others!

What is an ISA?

ISAs or individual saving accounts are government set-up products for you to save and invest your money. They’re fantastic and should be a part of everyone’s financial product portfolio in some capacity.

There are four main types of ISA which are:

- Cash ISAs – used primarily for savings

- Stocks and Shares ISAs – used primarily used for investing

- Lifetime ISAs – used primarily for first-time buyers and retirement savings

- Junior ISAs – used primarily for young children to save and invest

This article will only discuss Stocks and Shares ISAs and Lifetime ISAs because these are the only ISAs you can invest your money from.

If you’re wondering more about ISAs vs savings accounts, then we cover that in another article.

Stocks and Shares ISA

Pros

- Tax-free contributions of up to £20,000 ISA annual allowance – this resets each tax year which like a SIPP runs from April to April

- Access to global markets to invest in shares, funds and trusts

- Self-managed and expert-managed options to help different levels of investors

- Returns can vastly outweigh Cash ISA and standard savings accounts

Cons

- You may get back less than what you put in (this is the same as your pension pot)

- There are 1000s of options, and it can be overwhelming for beginners, so do your research

- There are fees for using them, albeit not that high

Lifetime ISA

Pros

- You can contribute £4000 per year as part of your overall £20,000 annual ISA allowance

- The government matches your contribution up to £1000 or 25% of anything you put in

- You can invest the money that’s in your Lifetime ISA to improve the overall amount

- You can earn up to £32,000 in government bonus over the account’s lifetime

Cons

- You can only use the money for your first home or for your retirement

- They are only available for people aged 18-39 to open

Heads up: the Government has confirmed the Lifetime ISA is being replaced by a First-Time Buyer ISA, with details announced in June 2026. The £4,000 limit and 25% bonus continue for now, and we will update this section once the new rules are confirmed.

There are many plus points to owning either a Stocks and Shares ISA or a Lifetime ISA. Next, we’re looking at the overall benefits and drawbacks of having an ISA vs SIPP.

Overall ISA Pros

- You can withdraw money from an ISA whenever you like

- Tax free savings

- You have control of where your investments go

- You don’t need to wait until you’re retired to enjoy the money

Overall ISA cons

- Max contributions of £20,000 a year vs £60,000 for a SIPP

- You’re putting in taxed earnings rather than untaxed ones if you pay into a SIPP

- No bonus on your contributions (other than a Lifetime ISA but only a max of £1000)

- You can not carry forward and unused allowance

Can I have an ISA and a SIPP?

Yes, you can. In fact, it’s often advised to hold both types of accounts as both offer tax-efficient ways of saving for your short term goals and for retirement.

If you’re just getting started and are unsure what to open, it’s advisable to seek professional help from a financial advisor.

SIPP Vs ISA - Who wins?

Honestly, for most people it is not a case of one beating the other. The smartest move is usually to use both, in this order:

- Take any workplace pension match first. If your employer matches your contributions, that is an instant return you cannot get anywhere else.

- Higher-rate taxpayer? Lean towards the SIPP. Thanks to tax relief, £100 in your pension pot costs a higher-rate taxpayer just £60. For a basic-rate taxpayer it costs £80.

- Might need the money before 55? Favour the ISA. Your cash stays flexible and you can withdraw it at any time, completely tax-free.

- Aiming to retire early? Use both. Build a Stocks and Shares ISA to bridge the years before your SIPP unlocks, then let the SIPP do the heavy lifting for later life.

Worked example: a basic-rate taxpayer pays in £80 and the government tops it up to £100. A higher-rate taxpayer reclaims more through self-assessment, so the same £100 in the pot can cost as little as £60. An ISA gives you no top-up, but every penny comes out tax-free whenever you want it.

The takeaway: if your money is sat in a general investment account (GIA) or a standard savings account, you are very likely paying tax you could legally avoid. At least one of these wrappers should be part of your plan.

FAQs

For most people, the answer is both. A SIPP wins on tax relief and is ideal for money you will not touch until retirement. An ISA wins on flexibility, because you can access it at any age, tax-free. If your employer matches pension contributions, start there, then split the rest based on when you are likely to need the money.

The main drawback is access. Your money is locked away until age 55, rising to 57 from April 2028. On top of that, only 25% comes out tax-free and the rest is taxed as income, contributions are capped at £60,000 a year, and you are responsible for choosing your own investments, which is not for everyone.

It usually refers to carry forward. If you have unused annual allowance from the previous three tax years, and you were a member of a pension scheme during that time, you can carry it forward and pay in more than £60,000 in a single year, as long as you have the earnings to support it.

Yes, you will need to declare your SIPP on your self-assessment tax return if you are a higher or additional rate taxpayer. This way, you can get your tax paid back to you. If you’ve yet to claim the additional rate, you can claim back the tax for the previous three tax years.

No, in fact if used together, you can receive tax relief on both accounts, plus have your employer pension contributions added on top.

Both offer useful tax advantages, but a SIPP gives you more control over where your money is invested. Equally, both invest via the stock market through an investment account.

If you are self-employed, however, a SIPP is your only option for a pension pot.

Any money paid into your SIPP will usually be passed onto a spouse when you die.

Yes. From April 2027 the cash ISA limit drops to £12,000 a year for under-65s, although the overall £20,000 ISA allowance is unchanged, and a 22% charge applies to interest on cash left uninvested in a stocks and shares, Lifetime or innovative finance ISA. The stocks and shares ISA limit stays at £20,000, so it remains a strong partner to a SIPP for tax-free investing. Separately, the Lifetime ISA is being replaced by a First-Time Buyer ISA, with details announced in June 2026. These plans are still subject to consultation.

SIPP or ISA - Roundup

The bottom line: a SIPP and an ISA are not rivals, they work as a team. The SIPP gives you bigger tax relief for the long haul, while the ISA keeps your money within reach whenever you need it.

Use the SIPP for retirement and lean on the ISA for everything before then. Just remember the SIPP stays locked until at least 55 (57 from April 2028), so plan your access around that.

Share this article with friends

Disclaimer: Content on this page is for informational purposes and does not constitute financial advice. Always do your own research before making a financially related decision.