Best Investing App For Beginners

Investing Made Simple | Wealthify

4.5

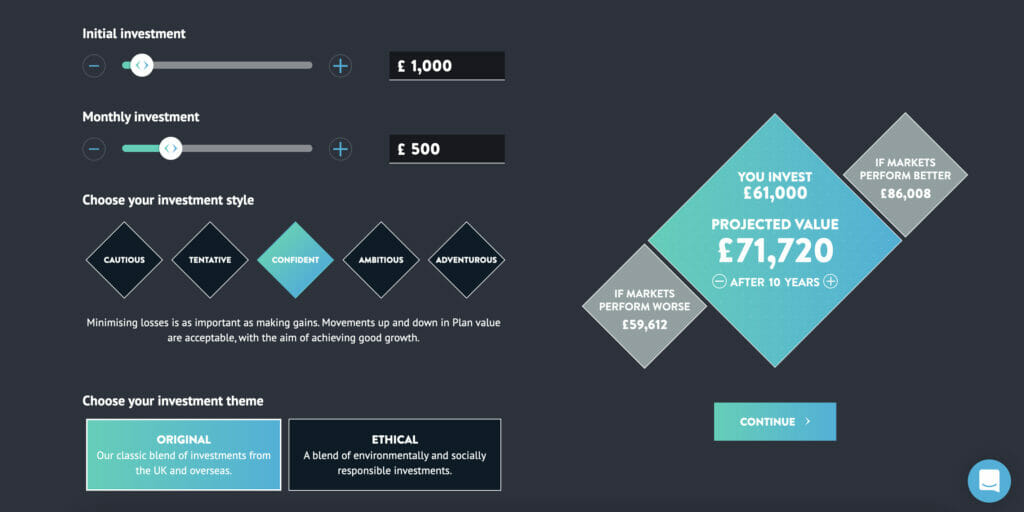

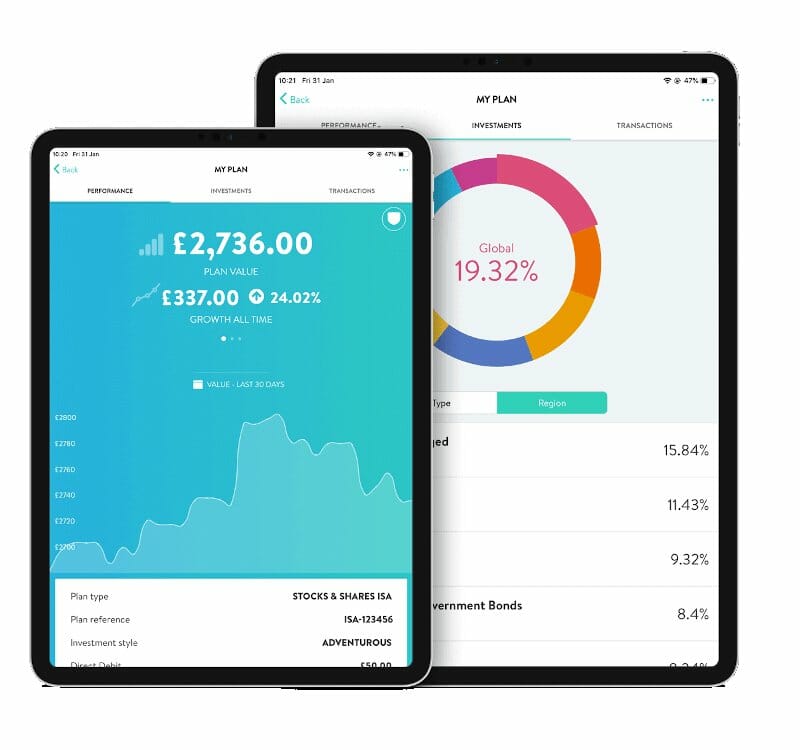

Popular robo-advisor with 5 expert-managed portfolios tailored to your investing style.

Pros:

- No minimum investment - portfolios start at £1

- Engaging app and user experience

- Charge a flat rate - keeping fees simple

Cons:

- Not for those who want to pick individual stocks

Your capital is at risk.

Wealthify Ratings

- Suitable For Beginners

- Useful Features

- Price / Fees

- Customer Service

- Customer Feedback

- User Experience

Best Investing App For Beginners

Investing Made Simple | Wealthify

4.5

Popular robo-advisor with 5 expert-managed portfolios tailored to your investing style.

Pros:

- No minimum investment - portfolios start at £1

- Engaging app and user experience

- Charge a flat rate - keeping fees simple

Cons:

- Not for those who want to pick individual stocks

Your capital is at risk.

Best Investing App For Beginners

Investing Made Simple | Wealthify

4.5

Popular robo-advisor with 5 expert-managed portfolios tailored to your investing style.

Pros:

- No minimum investment - portfolios start at £1

- Engaging app and user experience

- Charge a flat rate - keeping fees simple

Cons:

- Not for those who want to pick individual stocks

Your capital is at risk.

Best Investing App For Beginners

Investing Made Simple | Wealthify

4.5

Popular robo-advisor with 5 expert-managed portfolios tailored to your investing style.

Pros:

- No minimum investment - portfolios start at £1

- Engaging app and user experience

- Charge a flat rate - keeping fees simple

Cons:

- Not for those who want to pick individual stocks

Your capital is at risk.

Best Investing App For Beginners

Investing Made Simple | Wealthify

4.5

Popular robo-advisor with 5 expert-managed portfolios tailored to your investing style.

Pros:

- No minimum investment - portfolios start at £1

- Engaging app and user experience

- Charge a flat rate - keeping fees simple

Cons:

- Not for those who want to pick individual stocks

Your capital is at risk.